Last updated: 14 June 2026

By Stiv · Design, technology and personal finance

This is an opinion piece. Views expressed are the author's own and do not constitute professional or financial advice.

Cool Factor: 3/5

Fixed-for-life cover, a handy virtual GP, and a lot of phone calls.

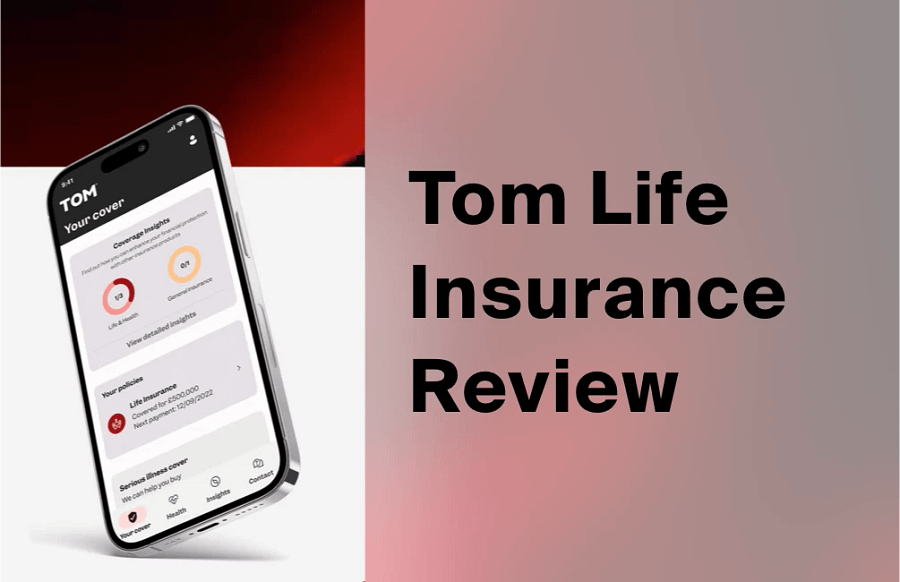

This is my honest Tom insurance review, written as an actual customer rather than someone skimming the marketing. I took out a lifetime serious illness cover policy with Tom, so this Tom insurance review is based on living with the application, the price and the perks, not on a press release.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

Want a Tom quote?

If this Tom insurance review has you ready to compare cover, you can start a quote through my referral link below. Meanwhile, the current offer and how it works sit on our Tom life insurance page.

Section 01 / The basics

What is Tom, and what did I buy?

A digital insurer built for UK families, and the serious illness policy I actually signed up for.

Tom is a digital insurance brand aimed squarely at UK families, best known for life insurance from a few pounds a month. Alongside straightforward life cover, it also offers serious illness cover, which is the product I bought. Mine is a lifetime serious illness cover policy that auto-renews monthly at the same premium, so the price I agreed at the start is the price I keep paying, which matters when you want certainty rather than a number that creeps up every year.

For the full factual breakdown of how Tom works, the cover types and the regulation, I have a separate reference page here: Tom life insurance: how it works. This piece, by contrast, is the opinion, the lived-in version.

Section 02 / Who you are buying from

The company and underwriter behind Tom

A slick consumer brand on the front, a Swiss Re-owned insurer doing the heavy lifting behind it.

It helps to know who you are actually buying from. Tom and TOM.co.uk are trading names of Candid Insurance Services Ltd, which is part of the Clark group and is authorised and regulated by the Financial Conduct Authority (FRN 603273). Candid arranges the cover; the policies themselves are underwritten by iptiQ, the digital insurer owned by Swiss Re.

That last point reassured me more than the branding did. When Swiss Re's iptiQ announced the tie-up, it framed the goal as joining forces with Candid to "provide affordable and accessible life insurance solutions to UK customers" through the Tom and Polly brands. In plain terms, a slick consumer front end sits on top of a serious, well-capitalised reinsurer. As a customer, I would rather the name behind my claim be Swiss Re than a start-up I had never heard of.

Section 03 / The why

Why I took out cover in the first place

This was personal, not a spreadsheet decision.

Honestly, it was personal. A close family member developed cancer young, and they did not have cover in place when it happened. As the main income for my household, that scenario sat with me. Through work I already have income protection, private health insurance and long-term sick cover, so the day-to-day was handled. What I did not have was a lump sum that would land if I were seriously ill, the kind of money that buys time and choices rather than just replacing a salary. That gap is what pushed me to a serious illness policy specifically, rather than plain life cover.

Section 04 / Sign-up

The application: more phone calls than I expected

The "covered in minutes" promise and my reality drifted a long way apart.

Here is where the "quick digital insurance" promise and my reality drifted apart. For me, the application was noticeably phone-heavy. There were several calls back and forth, a set of medical questions, and ultimately I had to obtain a GP report to share with the underwriter before things could be finalised. None of it was unreasonable for serious illness cover, especially given my family history, but it was a faff and it took longer than the breezy "covered in minutes" framing suggests.

To be fair to Tom, this is partly the nature of the product. The more a policy could pay out, and the more your medical background matters, the more underwriting it needs. A simple life quote for a healthy applicant can be near-instant; serious illness cover with a strong family cancer history is never going to be a two-tap job. Just go in expecting calls and paperwork, not a frictionless app journey.

Section 05 / Cover and price

The cover, and the fixed price for life

Not the cheapest, but the premium never moves, and that is the bit I rate most.

The cover itself is clear, which I appreciated. I knew what was and was not included, and the lifetime, fixed-premium structure means I am not bracing for an annual hike. The fixed price for life is the single best thing about the policy: the premium I agreed at the start never rises, which for lifelong cover is rare and genuinely reassuring. On price overall, though, I will be straight: it is not cheap for me. I am in my mid-thirties, and the underwriting clearly factored in the close family cancer history, so my premium sits well above the headline "from £5 a month" you see in the adverts. That figure is real for some people, but it is a floor for the youngest, healthiest applicants, not a typical price. Anyone with medical or family-history complexity should expect more.

Tax treatment and exactly what triggers a payout depend on your policy and circumstances, so read the documents rather than the marketing. For impartial, non-salesy guidance on how much cover you actually need, the MoneyHelper life insurance guide is a sensible starting point.

Section 06 / The perk

The virtual GP: a nice perk, not a dealbreaker

Useful when you need it, clumsy to switch on, and not the reason to buy.

The included virtual GP is the extra Tom leans on hardest, so it deserves an honest look. First, setting it up was a faff. The app and website simply say you will get an email invite from the partner that runs the service. Mine never arrived, so I had to chase Tom directly before it was sorted. They did fix it, but it felt clumsy and slow. In my view Tom should send the setup email and manage the redemption itself, rather than leaning on another service and leaving you waiting and wondering.

Once it was live, the service itself was good. I have used it once, when a false widow spider bite became infected, which is apparently an increasingly common problem in the UK. The GP was fast, courteous and helpful. I have not needed it since, though, so for me it is a nice extra rather than an essential.

There is also a catch worth flagging. A private GP means paying in full for any prescriptions, and for most everyday issues the edge is largely lost, because GP at Hand (formerly Babylon) does much the same thing on the NHS and lets you use NHS prescriptions. The real upside of Tom's GP, therefore, is speed: being able to talk to a doctor quickly when booking an NHS appointment is a struggle. That is useful, but it is not a reason on its own to buy the policy.

The product is better than its marketing.

Section 07 / The downsides

Honest criticisms: the calls, the setup and the branding

No Tom insurance review is worth much without the parts that grated.

First, the calls. The volume of follow-up contact during setup was relentless. I understand a serious illness application needs a conversation, so I am not complaining that they called at all; it is the frequency and persistence that wore thin. If you are someone who finds repeated insurance calls stressful, brace yourself.

Second, the virtual GP onboarding was needlessly clunky, as I describe above. Relying on a partner's email invite that never turned up, then making me chase it, is exactly the kind of friction a "digital-first" brand should design out.

Third, and this is subjective, the branding is not for me. Tom leans hard into an "insurance with dads in mind" identity, and that framing left me a little cold. It read as on-the-nose to me, with a faint whiff of the laddy, toxic-masculinity tone that some modern insurers chase to seem different. It did not stop me buying a policy, because the underlying product is solid, but it is the kind of marketing I personally find off-putting rather than charming. Some rivals push the provocative angle even harder, which I like even less, so Tom is far from the worst offender. It is just a style choice I would quietly prefer they dropped.

Worth stressing: these are presentation and process gripes, not product flaws. The cover does what it says.

Section 08 / Other reviews

How my experience compares to other Tom reviews

Strong public scores, with the same three gripes cropping up again and again.

To sense-check this Tom insurance review, I looked at the wider picture. Tom scores well publicly, rated "Excellent" at around 4.7 out of 5 on Trustpilot across several thousand reviews, with people praising clarity and helpful advisers. The recurring complaints from other customers cluster around three things: a lot of follow-up sales calls, occasional pushy selling, and unease about data being shared with insurance partners.

My experience only matched one of those. The calls, yes, absolutely. However, I did not feel pressure-sold at any point, and I have not had spammy third-party contact off the back of my quote. Communication was fast and easy whenever I needed it. So if the data-sharing horror stories are putting you off, my single data point is reassuring on that front, though I would still read the privacy notice before you hand over details.

Section 09 / The value

Is Tom worth it?

Yes for certainty and simplicity, less so if you only chase the lowest premium.

By the end of this Tom insurance review, my answer is yes, with caveats. The value is not in being the cheapest, because for my profile it is not. Instead, the value is in clear cover, a fixed lifetime premium, fast and easy servicing, and a virtual GP that is a nice extra once it is finally set up, all sitting on top of a Swiss Re-backed underwriter. If you want certainty and a tidy digital account to check in on, that is a fair package. If your priority is purely the lowest premium, get a few quotes and compare, because a broker or a different insurer might beat Tom on price for your circumstances. While you are sorting protection, it is also worth getting the rest of your affairs in order, a will being the obvious companion; our Farewill guide covers that side.

Section 10 / Alternatives

How Tom compares to the alternatives

A single-insurer app versus a whole-of-market broker or a comparison site.

It is worth being clear about what Tom is and is not. Tom is a direct-to-consumer brand, so you buy a single insurer's product through a slick app rather than comparing the whole market. A whole-of-market broker, by contrast, can line up several insurers and may undercut Tom for healthy applicants or trickier medical histories. Price-comparison sites can also surface cheaper term life cover, though they rarely match Tom's fixed lifetime premium or bundle in a virtual GP. Therefore, the honest framing is this: Tom suits people who value certainty, simplicity and a clean digital experience, while die-hard bargain hunters should still gather a few quotes elsewhere before committing.

Section 11 / Practical

Practical things to know

The boring but important bits: servicing, protection and the small print.

This Tom insurance review would not be complete without the boring but important details. Day-to-day, Tom is digital-first for servicing: you manage the policy and message the team online rather than through a phone line, even though the setup itself was phone-led for me. Cover is underwritten by an FCA-regulated insurer named in your documents, and eligible claims fall under the Financial Services Compensation Scheme if the insurer cannot pay. Read your policy schedule for the exclusions, the definitions that trigger a serious illness payout, and any cooling-off period before you commit, because those details matter far more than any advert.

Better than its marketing

To close this Tom insurance review out, Tom does the important job well: clear cover, a fixed lifetime price that never rises, and quick servicing. The virtual GP is a nice perk once you get past the clumsy setup, not a core reason to buy. It loses marks for too many phone calls, a GP onboarding that made me chase a third party, and branding that tries too hard.

Cool Factor: 3 out of 5

Cool Factor

★★★☆☆

3 out of 5

Overall, this Tom insurance review lands at a fair 3/5 Cool. Tom got the fundamentals right for me, clear serious illness cover at a fixed lifetime premium that never rises, which is why it is a solid "does the job" rather than a regret. It did not climb higher because the application needed too many calls, the virtual GP setup meant chasing a third party, and the "insurance for dads" branding leaves me cold. So if you can look past the marketing and you value certainty over the lowest price, it is worth a quote; just go in expecting a phone-led sign-up rather than a two-minute app.

Frequently asked questions

Is Tom life insurance any good?

In this Tom insurance review, the product proved solid: clear cover, a fixed-for-life premium and a handy virtual GP, underwritten by Swiss Re's iptiQ. The main downsides are a phone-heavy sign-up, a clunky GP setup and marketing that will not be to everyone's taste. Publicly, Tom rates around 4.7 out of 5 on Trustpilot.

Who underwrites Tom, and is it regulated?

Tom is a brand of Candid Insurance Services Ltd, authorised and regulated by the FCA (FRN 603273). The cover is underwritten by iptiQ, the digital insurer owned by Swiss Re. The specific insurer for your policy is named in your documents.

Does Tom offer serious illness cover or just life insurance?

Both. Tom is best known for life insurance, but it also offers serious illness cover, which is what I bought as a lifetime policy with a fixed monthly premium. Check the current product range and definitions on Tom's site, as these can change.

How much does Tom cost?

Adverts say from £5 a month, but that is a floor for the youngest, healthiest applicants. My premium is well above that because of my age and a close family cancer history. The good news is that the price is then fixed for life. The only way to know your number is to complete a quote, and it is worth comparing against other insurers or a broker.

Will Tom call me a lot after a quote?

In my case, yes. The follow-up calls during setup were persistent. I did not experience pushy selling or third-party spam, but the volume of calls was the most frustrating part of the process, so be ready for that.

More from CoolCuration

- Best pet insurance UK: if pets are part of the family, here is our honest comparison from real owners.

- Best UK savings accounts: build the emergency fund that sits behind any protection policy.

- Simplyhealth health plans: everyday health cover for the whole household, including dental and optical claims.

- Meela therapist matching: talking support if a diagnosis or money worry is weighing on you.

- Emma app: see your premiums and household spending in one tidy place.

This is an opinion piece reflecting my own experience as a Tom customer and is not financial or insurance advice. Cover, prices, definitions and exclusions are set by Tom and the underwriter and can change, so always read your policy documents and consider impartial guidance from MoneyHelper or a qualified adviser. CoolCuration is not authorised by the Financial Conduct Authority. This article contains a referral link; if you sign up through it, CoolCuration may receive a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

What's trending

Recent posts

- Best Free Budgeting Apps UK 2026

The best free budgeting apps in the UK for 2026, compared: what each free tier really includes, what is paywalled, and who each app suits.

The best free budgeting apps in the UK for 2026, compared: what each free tier really includes, what is paywalled, and who each app suits. - InvestEngine Review: My Honest Take After Six MonthsMy honest InvestEngine review after six months: no-fee ETF investing, the real bonus odds, and who this low-cost UK platform actually suits.

- Best Current Account UK 2026: Ranked and ComparedCurrent accounts2026 Edit The best current account is the one you actually enjoy opening Picking the best current account in 2026 is no longer just about interest. It is about the app you tap ten times a day, the perks that quietly pay you back, and the switch bonus that lands in a week. So… Read more: Best Current Account UK 2026: Ranked and Compared

No Comments.