Last updated: 18 June 2026

By Stiv · Design, technology and personal finance

This Tembo Money review is based on my own use of Tembo, which I first downloaded in November 2021, back when it was still Nude. For context, I have also overpaid my Nationwide mortgage through Sprive since October 2021. So I have lived with rival money apps for years, not days.

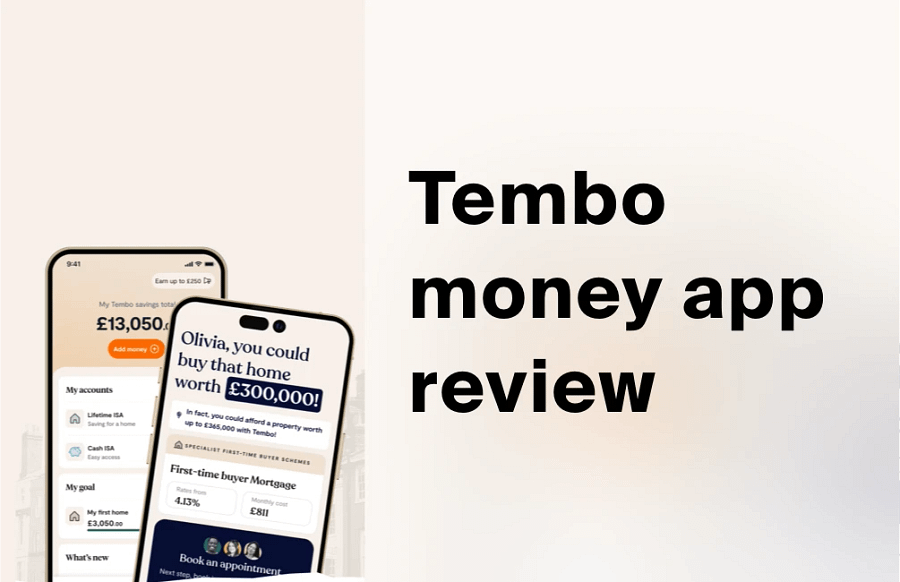

Welcome to my Tembo Money review, written after years of real use rather than a quick weekend trial. Tembo is a UK savings and mortgage app. I have watched it grow from the old Nude app into one of the slickest finance apps around. So this Tembo Money review reflects ongoing, hands-on use, not a press release.

This is an opinion piece. Views expressed are the author's own and do not constitute professional or financial advice.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

Cool Factor

★★★★★

5 out of 5 (Ice cold)

Your home may be repossessed if you do not keep up repayments on your mortgage. Tembo also offers a Stocks and Shares Lifetime ISA, where your capital is at risk. I cover both honestly below.

Want the Tembo sign-up reward?

First, the current Tembo offer and the qualifying steps live on our dedicated Tembo page. We keep the small print up to date there too.

What is Tembo Money?

Tembo Money is a UK savings and mortgage app, built around one clear idea. It helps people save a deposit faster, then buy a home sooner. In other words, it joins the saving and the buying into a single journey. For this Tembo Money review, that joined-up approach is the headline.

The range is broad for a young fintech. First, there is the HomeSaver account, an easy-access savings account with a market-leading headline rate. Next come two Lifetime ISAs, in cash and in stocks and shares. Both carry the 25% government bonus. In addition, Tembo offers an easy-access Cash ISA. There is also a one-year fixed-rate Cash ISA, provided by Investec. Finally, it runs an award-winning mortgage brokerage. That covers first-time buyers, home movers, remortgagers, buy-to-let and over-50s lending.

One quick clarification, because it matters. Tembo does not currently offer a standalone SIPP or personal pension. Instead, the Lifetime ISA is its retirement-friendly wrapper. You can use a LISA for a first home, or for later life from age 60.

The company behind Tembo Money

Trust matters in finance, so the company context belongs early in any honest Tembo Money review. Tembo was founded during the pandemic by Richard Dana. He previously worked as CFO at venture builder Founders Factory. Tembo Savings Limited runs the savings and ISA side. The Financial Conduct Authority authorises and regulates it (FRN 928010). Meanwhile, the mortgage and insurance advice sits under Tembo Money Limited (FRN 952652).

The track record is strong. Tembo has won UK's Best Mortgage Broker at the British Bank Awards five years running, from 2022 to 2026. It also won Best Lifetime ISA at the Good Money Guide Awards in 2023. Moreover, more than 400,000 savers now use the app. Tembo also quotes an average affordability boost of around £82,000 for mortgage customers.

Richard Dana is candid about why the app exists. "Getting a foot on the property ladder has never been harder, but there has been a much-needed influx of innovation in the market in recent years," he told Financial Reporter in 2024. That mission shows up in the product design.

First impressions and setup

Honestly, setup is where Tembo first won me over. Signing up was super smooth, super slick and super simple, which is rare for a finance app. First, you download the app. Then you answer a short set of questions. After that, you can open an account and fund it within minutes.

The onboarding never felt heavy. Identity checks ran quickly, the language stayed plain, and the interface guided me without jargon. As a result, the whole thing felt closer to a well-made consumer app than a stuffy bank. For me, that polish matters in this Tembo Money review. After all, friction is what usually puts people off saving.

The HomeSaver account I actually use

Let me be specific about what I personally use. My account is the Tembo HomeSaver, not an ISA. It is an easy-access savings account. You can hold up to £20,000, and there are no withdrawal limits.

The headline is a market-leading 5.55% AER. However, the structure deserves a clear explanation. The underlying base rate is 3.00% AER (variable). On top, a 1.55% AER fixed bonus applies for the first 12 months, which lifts the rate to 4.55%. Then a further conditional 1.00% AER bonus, fixed for a year, takes it to 5.55%. Tembo only pays that final bonus if you complete a mortgage through it within three years.

In plain terms, you earn 4.55% straight away. Then you unlock the full 5.55% by using Tembo's mortgage service. That is a smart hook, and it is honest on the page, but it is not automatic. So if you never take a Tembo mortgage, you simply keep the variable base rate. You do not get the full headline figure.

On safety, my HomeSaver money is held on trust and placed with Lloyds Bank plc, Tembo's deposit-taking partner for this account. The full detail sits in Tembo's HomeSaver Summary Box. Eligible deposits are protected up to £120,000 per eligible person per UK-authorised bank, building society or credit union by the FSCS (since 1 December 2025). Because the cash is pooled in trust, an FSCS payout could take up to three months. Rates are variable, so always check the live figure first.

Tembo's wider savings range

Beyond HomeSaver, the wider range is where Tembo flexes. The Cash Lifetime ISA currently pays 4.30% AER (variable). It suits first-time buyers aged 18 to 39 saving a deposit. Crucially, the government adds a 25% bonus on contributions. That is up to £1,000 a year on the £4,000 LISA limit. That limit sits inside your overall £20,000 annual ISA allowance.

There is a trade-off, though, and I will not gloss over it. The first-home price cap is £450,000, and retirement access starts at age 60. Withdraw for any other reason, and a 25% government charge applies. Because that charge hits the full amount withdrawn, you can get back less than you paid in. Tax treatment depends on the individual circumstances of each client and may be subject to change in future.

For investors, Tembo also offers a Stocks and Shares Lifetime ISA, which invests through a BlackRock MyMap fund. Naturally, this is an investment product, so capital is at risk. Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results. Eligible investments are protected up to £85,000 per person per FCA-authorised firm by the FSCS.

On cash ISAs, the easy-access Cash ISA pays up to 4.05% AER (variable). There is also a one-year fixed-rate Cash ISA at 4.60% AER (fixed) for new customers, provided by Investec. Personally, I keep my full ISA allowance for investing elsewhere. I also hold my own Lifetime ISA with JPMorgan Personal Investing rather than Tembo. That is simply how my pots are split, not a knock on Tembo.

The mortgage service and best-deal guarantee

Although I save with Tembo, I have not yet remortgaged through it, so I will be transparent. I used Sprive for my own overpayments this time around. Even so, the mortgage proposition looks excellent, and its reputation is well earned.

Tembo Mortgages is a whole-of-market broker. It has access to over 100 lenders and around 25,000 products. It specialises in boosting affordability, including income-boost and guarantor options for first-time buyers. On fees, a standard mortgage costs £499. A Boost or complex case costs £749, payable only once you have an offer. Helpfully, savers can also get fee-free mortgage advice, subject to eligibility.

The headline reassurance is the Best Mortgage Deal Guarantee. Essentially, find a cheaper comparable deal from another whole-of-market adviser, and Tembo says it will pay the difference. Terms apply, of course. Your home may be repossessed if you do not keep up repayments on your mortgage. Also, Tembo, not CoolCuration, gives the regulated advice. CoolCuration is not authorised by the FCA.

Customer service in my experience

Customer service is often where finance apps fall down, so I tested it. In my experience, Tembo's support held up well. I emailed them with questions about the product range and withdrawal times. The replies came back fast, clear and friendly.

Tembo says its support team is UK-based and available seven days a week. That matched my reality. Withdrawals landed quickly, exactly as described, with no surprise holds. Consequently, I never felt left guessing. That is more than I can say for some bigger banks I have used.

The Tembo referral offers explained

There are two separate Tembo referral schemes, and people often muddle them. So this Tembo Money review spells out both clearly. I have not personally referred anyone yet. Even so, the terms are published on Tembo's site.

The savings referral pays a matching reward of between £10 and £1,000. To qualify, your friend signs up through your link as a new customer. Then they open a new Tembo Cash ISA or Lifetime ISA, or transfer one in. Finally, they pay in £500 or more within 30 days. I would aim for £501 to be safe. Importantly, Tembo allocates the reward randomly from set probabilities. Higher amounts are rare, so most people land nearer the £10 end. Treat the £1,000 as a long shot, not a promise, and never as free money. Rewards cover up to five completed referrals per month.

The mortgage referral works differently. Here, your friend mentions your name and registered email on their first Tembo call. Then, once they complete on a mortgage arranged by Tembo, you both receive up to £100 each. There is no cap on the number of friends you can refer.

To keep this independent, our own Tembo referral details live on our Tembo page. We update that page separately from this opinion piece.

Honest critical observations

No review earns a 5/5 without naming what stops it being perfect. This Tembo Money review is no exception. So here is where I push back.

First, the headline HomeSaver rate is conditional. You only bank the full 5.55% AER if you complete a mortgage through Tembo within three years. Otherwise, you keep the lower variable base. That is fair, and Tembo discloses it clearly. Even so, it is not the simple "5.55% on your cash" some people assume.

Second, Tembo is app-only. There is no web dashboard and no branch. That will not suit everyone, particularly anyone who dislikes managing money on a phone. Third, the savings rates are variable, so today's market-leading number can move. Fourth, eligibility has real limits. The Lifetime ISA is 18 to 39 only. Plus, the 25% withdrawal penalty can leave you worse off if you dip in early.

Finally, partner banks hold your savings, rather than Tembo directly. Mortgage outcomes also depend on your circumstances and the fee. None of these are dealbreakers for me. However, they are the honest caveats that any balanced Tembo Money review must include.

Why Tembo matters now

Context helps explain the score. UK first-time buyers face a brutal affordability gap. Saving a deposit while rents stay high is properly hard. Against that backdrop, an app that pays a strong rate and then helps you actually buy is timely.

Richard Dana frames the founding story neatly. "I set up Tembo during covid (Tembo means elephant in Swahili, because the elephant is the most family minded animal on the planet) with the aim of trying to find alternative ways for families to help their loved ones to buy their first home," he told Financial Reporter. That family-first, buy-sooner mission still runs through every screen. Partly, that is why this Tembo Money review lands where it does.

Value for money: first-time buyer versus remortgager

So, who is it actually for? For a first-time buyer, I think Tembo is brilliant. Honestly, I am a little jealous, because Nude launched after I bought my first place. You get a competitive savings rate, the LISA bonus and a specialist broker. All of it sits in one app. If I were starting out today, I would happily point a friend towards it.

For a remortgager, the case is strong too, though I rate it on reputation rather than personal use here. The five-year award streak and the best-deal guarantee are reassuring. That said, I would still compare brokers first. Our guide to the easiest mortgage broker in the UK is a sensible starting point.

On the savings side, Tembo is not the only option, and I would not pretend otherwise. For the wider picture, see our roundup of the best savings accounts in the UK. We also cover the best savings options this tax year. Then, once you have a mortgage, an app like Sprive can help you overpay and clear it faster. I explain more in our guide to how Sprive works. Overall, for value and execution, Tembo holds its own comfortably.

The verdict

Cool Factor

★★★★★

5 out of 5

So here is my verdict. In my experience, Tembo is one of the slickest finance apps I have used. So it earns a 5/5 Ice cold. The rates are competitive and the setup is effortless. Support is helpful, and the product range is unusually broad for the category. Above all, it does one thing properly: it helps you save, then helps you buy.

Overall, this is a confident 5/5 Ice cold in my book. Tembo blew me away with its speed, clarity and laser focus on homebuying. The award-winning mortgage service backs that up. It is not flawless. The headline rate is conditional, it is app-only, and rates can move. Even so, none of that knocks it off top spot for me. Years on from the Nude days, Tembo remains the rare money app I am happy to keep open. That is exactly why this Tembo Money review ends on full marks.

Tembo Money review FAQs

Is Tembo Money worth it?

In my experience, yes, especially if you are saving for a first home or planning a mortgage. You get a competitive, FSCS-protected savings rate. You also get access to an award-winning broker in one app. As always, though, this is my opinion and not financial advice, so check the current terms yourself.

What interest does the Tembo HomeSaver pay?

The headline is 5.55% AER. That is a 3.00% AER variable base, plus a 1.55% AER fixed 12-month bonus (which together make 4.55%), plus a conditional 1.00% AER bonus. Tembo pays that final bonus only if you complete a mortgage through it within three years. Because the base rate is variable, always confirm the live figure first.

Is my money safe with Tembo?

Your savings sit with Tembo's FSCS-protected partner banks. HomeSaver money is currently placed with Lloyds Bank plc, on trust, so eligible deposits are protected up to £120,000 per eligible person per UK-authorised bank. In addition, Tembo Savings Limited is FCA authorised (FRN 928010). Tembo Money Limited is authorised for mortgage advice (FRN 952652).

How much is the Tembo referral bonus?

The savings referral pays a random matching reward of between £10 and £1,000. However, most people receive an amount near the lower end. Separately, the mortgage referral pays you and your friend up to £100 each once they complete a Tembo mortgage. Treat the top figures as rare, not guaranteed.

How does Tembo compare to Sprive?

They do different jobs, really. Tembo helps you save a deposit and arrange a mortgage. Sprive, by contrast, helps you overpay and clear an existing mortgage faster. Personally, I save with Tembo and overpay my Nationwide mortgage through Sprive, so I happily use both.

Does Tembo charge mortgage fees?

Yes, usually. A standard mortgage costs £499. A Boost or complex case costs £749, payable only once you have an offer. However, eligible savers can get fee-free mortgage advice, so it is worth checking your eligibility first.

More from CoolCuration

- When to remortgage in the UK: work out the right moment to switch before your fixed rate ends.

- JPMorgan Personal Investing review: my take on the ready-made portfolio service where I hold my own Lifetime ISA.

- Chip auto-saving app: automate your deposit saving and grab the referral code.

- Chase refer a friend code: get £50 when you pay in, handy for parking deposit cash and earning interest.

- New home gift guide: once you have the keys, ideas to make the place feel like yours.

Disclaimer

This Tembo Money review is an opinion piece for general information only and is not financial advice. Rates, bonuses, eligibility and offer terms are variable and can change or be withdrawn. Always check the latest details on Tembo's site before applying. Eligible deposits are protected up to £120,000 per eligible person per UK-authorised bank, building society or credit union by the FSCS (since 1 December 2025). Eligible investments are protected up to £85,000 per person per FCA-authorised firm. Capital at risk applies on any Stocks and Shares Lifetime ISA. The value of investments can go down as well as up and you may get back less than you invested. A 25% government withdrawal charge may apply on unauthorised Lifetime ISA withdrawals. That can mean getting back less than you paid in. Tax treatment depends on the individual circumstances of each client and may be subject to change in future. Your home may be repossessed if you do not keep up repayments on your mortgage. You should consider speaking to a qualified adviser before making financial decisions. CoolCuration is not authorised by the Financial Conduct Authority. This article contains affiliate or referral links. If you sign up through them, I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

What's trending

Recent posts

- Tembo Money Review UK

My honest Tembo Money review after years of real use: HomeSaver rates, Lifetime ISAs, the mortgage service and the referral, tested for UK savers.

My honest Tembo Money review after years of real use: HomeSaver rates, Lifetime ISAs, the mortgage service and the referral, tested for UK savers. - Tom Insurance Review (UK): My Honest TakeLast updated: 14 June 2026 By Stiv · Design, technology and personal finance This is an opinion piece. Views expressed are the author's own and do not constitute professional or financial advice. Cool Factor: 3/5 Tom insurance review2026 Edit Fixed-for-life cover, a handy virtual GP, and a lot of phone calls. This is my honest… Read more: Tom Insurance Review (UK): My Honest Take

- Wype Original vs Soothe: Which Should You Buy?Wype just dropped a new Soothe gel for sensitive skin. I've used Original for a year and Soothe for three months, so here's the honest, first-hand verdict on which to buy. #Wype #EcoBathroom #SustainableLiving #WetWipeAlternative #PlasticFree

No Comments.