Last updated: 19 April 2026

By Stiv · Design, technology and personal finance

This is an opinion piece. Views expressed are the author's own and do not constitute professional advice.

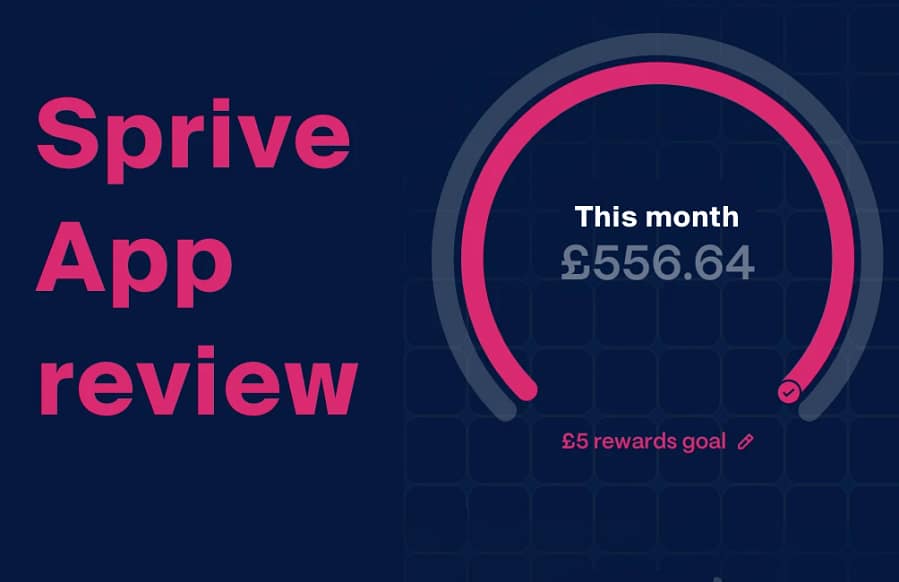

I've been using Sprive with my Nationwide mortgage since October 2021, making £100 monthly overpayments through the app's auto-save feature. In that time I've overpaid a total of £3,294.55, including cashback from Shop with Sprive on our weekly shops. This review is based on over four years of real, daily use.

If you're looking for a realistic way to make progress on your mortgage without committing to rigid overpayments, the Sprive mortgage app is one of the better-known tools in the UK. This Sprive mortgage app review focuses on what actually matters: how it works in day-to-day use, who it's good for, and where it falls short. It's not a sales pitch, and it's not a deep dive into regulation or bonuses. If you're mainly concerned about security and FCA regulation, we cover that separately: Is Sprive safe?

Cool Factor

★★★★☆

4 out of 5

What is Sprive?

Sprive is a UK app designed to help homeowners make small, consistent mortgage overpayments and boost them with cashback. It works by connecting to your bank via Open Banking, analysing your transactions, and setting aside small, affordable amounts you won't miss. You choose a minimum and maximum saving level (the minimum is set at £25). Overpayments are then made according to your setup and your lender's process.

You stay in full control throughout. You can pause, change the frequency, or withdraw the money at any time. It's more like a smart, automated savings tool that happens to send your savings straight towards your mortgage rather than into a regular account.

On top of that, there's a cashback feature called Shop with Sprive. When you shop with over 1,000 partner retailers, a percentage of your spend is added to your overpayment pot, effectively helping you chip away at your mortgage while you buy your usual groceries, clothes, or takeaways. For a deeper look at how the cashback side works in practice, our Sprive cashback explained guide covers checkout tips, rates, and when it's genuinely worth the effort.

First impressions

I first downloaded Sprive in October 2021 after seeing it mentioned on a finance forum. Setting it up took under ten minutes: connect your bank, confirm your mortgage details with Nationwide, and set your saving level. I was genuinely surprised at how slick, simple, and secure the process felt.

Within the first week, the app had quietly built up about £30 from spare cash based on my spending patterns. I sent that as an overpayment to Nationwide through the app and got confirmation from both Sprive and my bank. That double-confirmation was reassuring because it meant I could track what happened on both sides, not just inside the app.

The onboarding didn't try to upsell me on anything or push me towards a specific saving level. It just asked what I could afford, set the limits, and got on with it. For a full walkthrough of the setup mechanics, our how the Sprive app works guide covers each step.

The experience: four years of daily use

Over four years of using Sprive, the thing that's genuinely impressed me is how invisible it becomes. I set up a £100 monthly auto-save early on and have barely touched the settings since. Some months I can afford more, and Sprive nudges the amount up within my limits. Other months are tighter, and it stays closer to the minimum. That flexibility is the core difference between Sprive and a fixed standing order.

Before Sprive, I had a simple standing order for an extra £100 a month. The problem was that some months I could easily afford it, and others it left me short. That's where Sprive genuinely shines. It's smart, not static. It adjusts based on your spending, so you're never over-committed.

The cashback side

The Shop with Sprive feature has added a nice bonus, especially on weekly supermarket shops. I buy Tesco or Sainsbury's gift cards through the app at checkout and the cashback feeds directly into my mortgage pot. Over four years, the cashback has contributed a meaningful chunk of my total £3,294.55 in overpayments. It's not life-changing money on its own, but it compounds over time.

The rates vary by retailer, typically between 1% and 4%. It's not always the best rate compared to a dedicated cashback platform like TopCashback, but the convenience of having it go straight to your mortgage means I actually use it consistently, which is the whole point.

The overpayment tracking

Sprive shows you projected savings in interest and time based on your overpayment history. I also cross-reference this with the Monzo overpayment calculator, and the numbers have consistently lined up. Seeing the projected months knocked off your term is genuinely motivating, even when the individual amounts feel small.

Where Sprive falls short

No app is perfect, and after four years I've found some genuine frustrations:

- Bank connection refreshing. My Nationwide connection needs re-authorising roughly every 90 days. This is an Open Banking quirk rather than a Sprive problem, but it's still annoying when the app stops working and you don't notice for a week.

- Cashback retailer range. The catalogue has grown significantly (now over 1,000 brands), but I'd still like to see more supermarket options and better rates on everyday shops. The best cashback percentages tend to be on retailers I don't use regularly.

- Less value if you're already disciplined. If you're the kind of person who sets up a standing order and never misses it, Sprive's automation doesn't add much. The app solves a behavioural problem, and if you don't have that problem, it's unnecessary overhead.

- Overpayment limits are your responsibility. Sprive doesn't automatically know your lender's annual overpayment allowance. You need to check this yourself and set your limits accordingly. Our Sprive overpayment rules guide explains what to check.

Value for money

Sprive's core features are free. There's no subscription fee for autosaving, overpayments, basic mortgage tracking, or cashback. The company makes money from remortgage commissions (when users switch deals through the app's broker service) and from a share of the gift card cashback revenue. For a full breakdown of the business model: how does Sprive make money.

In practical terms, Sprive costs you nothing and has helped me overpay £3,294.55 over four years. Even accounting for the time spent buying gift cards at the checkout, the return on effort is comfortably positive. If you're comparing it to the cost of a mortgage broker or financial adviser, there's no contest. For the comparison with just doing it yourself, our Sprive vs manual overpaying guide covers the trade-off honestly.

The verdict

For the right person, Sprive is genuinely worth it. It's not about beating the system or finding loopholes. It's about making good behaviour easier. If you want to overpay your mortgage but struggle with consistency, Sprive can help, and the cashback feature is a nice bonus that compounds over time.

After four years and over £3,200 in overpayments, I'm still using it. That says more than any feature list.

Cool Factor

★★★★☆

4 out of 5

Overall, a solid 4/5 Stone cold. Sprive has genuinely changed how I manage my mortgage, and the combination of autosaving and cashback has produced real, measurable results over four years. It didn't quite hit Ice cold because the bank connection refreshing is a persistent annoyance, the cashback rates on everyday shops could be better, and the app adds less value if you're already disciplined with manual payments. But for the majority of homeowners who intend to overpay but never quite get around to it, Sprive turns that intention into action, and that's worth a lot.

If you want to try it, the current sign-up bonus and claiming steps are on our referral page:

Get the current Sprive referral bonus

For the trust and regulation breakdown: Is Sprive safe?. For a step-by-step setup walkthrough: How the Sprive app works.

FAQs

Is the Sprive app worth it?

If you struggle with consistency, yes. Over four years I've overpaid £3,294.55 through the app, including cashback, without ever having to remember to make a manual payment. If you're already disciplined with a standing order and don't care about cashback, the app adds less value. Our Sprive vs manual overpaying comparison covers this in more detail.

Is Sprive free to use?

Yes. The core features are free. Sprive makes money from remortgage commissions and a share of cashback revenue, not from user subscriptions. For the full breakdown: how does Sprive make money.

Is Sprive safe?

Sprive is FCA-registered (FRN: 919863), uses Open Banking (so it never sees your bank password), and holds your funds via a safeguarded e-money provider. Safeguarding is not the same as FSCS protection, which is an important distinction. Our is Sprive safe guide covers FCA status, Open Banking security, and fund protection in plain English.

How much can I save by overpaying with Sprive?

It depends on your balance, rate, and how much you overpay. As a rough example, on a £200,000 mortgage at 4.3% over 25 years, overpaying £100 a month could save around £20,000 in interest and knock roughly four years off the term. Sprive has an in-app calculator that models your specific numbers, and you can cross-reference with the MoneySavingExpert overpayment calculator.

Does Sprive work with Nationwide?

Yes. I've been using it with Nationwide since October 2021. The connection occasionally needs refreshing (roughly every 90 days), which is a standard Open Banking behaviour rather than a Sprive issue. Overpayments show up on my Nationwide statement within a couple of working days.

How does Sprive compare to a standing order?

A standing order is fixed and predictable: the same amount leaves your account every month regardless of your situation. Sprive is flexible and adjusts based on your spending. If your outgoings vary month to month, Sprive is easier to live with long term. If your income and spending are rock-steady, a standing order may be all you need.

More from CoolCuration

- Best mortgage overpayment apps UK – how Sprive compares to Chip, Plum, Emma, and other tools.

- Octopus Energy referral guide – switch energy provider and pick up bill credit to free up cash for overpayments.

- Chip app – automate savings with FSCS protection if you'd rather build a pot before overpaying.

- Gifts for techies – curated picks for people who love a smart gadget.

- Pixel Watch 4 – smart health tracking that pairs well with an optimised life.

This review is an opinion piece and does not constitute financial advice. CoolCuration earns from referral links, which are clearly disclosed. Our editorial opinions are never influenced by these partnerships. Always check your mortgage terms, overpayment limits, and the app's current features before making decisions.

No Comments.