Last updated: 21 June 2026

By Stiv · Design, technology and personal finance

Welcome to my updated Autopilot app review from a UK perspective, with performance as at 21 June 2026. Two months ago I was sitting on a tidy gain. Since then, I have sold out of one folio entirely, doubled down on another, and watched a third quietly surge. Same app, same dual-app setup, yet a very different portfolio. If you ever wanted proof that copy trading is a bumpy ride, this Autopilot app review is it.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

This is a personal account of my own experience and does not constitute financial advice.

Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results.

This is an opinion piece. Views expressed are the author's own and do not constitute professional advice.

This Autopilot app review is based on ten months of personal use since 11 August 2025, copy trading through a Robinhood UK account with real money on the line. Every number, friction point and verdict below comes from my own portfolio.

Cool Factor: 2/5

Want to try copy trading via Robinhood UK?

Autopilot cannot run without a connected broker, and Robinhood UK is the account I use for it. Your capital is at risk, and the latest sign-up terms sit on our referral page.

What is the Autopilot app?

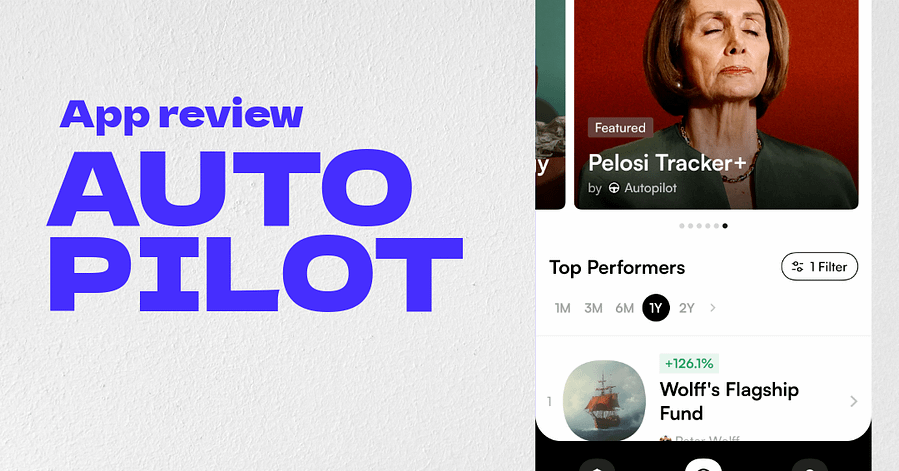

Before diving deeper into this Autopilot app review, here is a quick recap. Autopilot is a US-based copy-trading app. Essentially, it lets you mirror the portfolios of well-known investors, politicians and hedge-fund managers. Moreover, the team behind the viral Pelosi Tracker account on X built Autopilot. Since launching in 2023, the company says it has grown quickly, with billions of dollars in connected assets across its user base.

However, Autopilot itself is not a brokerage. Instead, it connects to your existing broker and places trades on your behalf. In other words, the app proportionally matches the moves of whichever folio (its term for portfolio) you choose to follow.

Popular folios include Pelosi+ (formerly the Pelosi Tracker) and the Inverse Cramer, alongside hedge-fund trackers and, more recently, AI-led and thematic portfolios. Each folio requires a $500 minimum investment, while annual access starts at $99.99. Importantly, Autopilot Advisers LLC is registered with the US Securities and Exchange Commission as an investment adviser. For UK investors, though, that means Autopilot itself sits outside FCA jurisdiction.

Setting up as a UK investor

Getting started with Autopilot from the UK takes a little effort. Firstly, you cannot just download a single app. Because Autopilot needs a connected US brokerage, I first opened a Robinhood UK account. Robinhood U.K. Ltd is authorised and regulated by the Financial Conduct Authority (FRN: 823590), so that side feels reassuringly above board. Verification was quick. You also need to complete a W-8BEN tax form, since you will be accessing US securities. If you are brand new to all this, my guide on how to start investing in the UK is a calmer place to begin.

Once Robinhood was set up, I downloaded Autopilot separately and linked the two together. This is where the friction begins. Specifically, you must authorise Autopilot to act on your Robinhood account. Currently, every trade still needs manual approval before it executes on the Robinhood side. In theory, that gives you more control. In practice, miss a notification and you miss a trade.

The annual subscription costs $99.99, charged in USD. Therefore, I paid via my Wise multi-currency account. Wise gave me a competitive exchange rate. It also doubles as a handy holding place for any USD dividends or withdrawals. In my experience, a Wise account is practically essential if you plan to use Autopilot from the UK.

Ten months of copy trading

I signed up on 11 August 2025. Then I put $500 into each of three folios: Pelosi+, the Jim Simons Tracker and the Inverse Cramer. That made $1,500 as a starting pot, the minimum across all three. Since then, I have added roughly $100 to each active folio every month.

The method is simple in theory. Each month, I deposit around £300 from my Monzo account straight into Robinhood. Because Robinhood only accepts GBP deposits, it then handles the conversion to USD. After that, I open Autopilot and assign the funds. Autopilot then auto-trades in the background based on each folio's strategy.

Simple enough, but expect a barrage of Robinhood notifications. Indeed, each trade triggers at least one alert. As a result, I turned mobile notifications off fairly quickly.

Trade delays explained

Trade delays caught me off guard early on. Notably, they vary a lot by folio. Pelosi+ operates around two weeks behind congressional disclosure filings. The Inverse Cramer, by contrast, trades without a delay, although it rebalances every three months. Consequently, your entry price often differs sharply from the headline numbers. That gap explains much of why my own returns swing so widely.

The Pelosi situation

Nancy Pelosi announced her retirement from Congress in November 2025. That threw a spanner in the works for anyone copying her trades. Since then, Autopilot has transitioned the folio into a broader congressional portfolio, rebranded as Pelosi+. Initially, I wondered whether to pull my money out. After all, the whole appeal was tracking one specific (and controversially successful) trader. However, Pelosi+ has since become my single biggest Autopilot holding, for reasons I will come to.

Why I sold out of the Jim Simons folio

Here is the biggest change since my last Autopilot app review. As of 21 June 2026, I have sold out of the Jim Simons Tracker completely. I exited at roughly +1.5%, so a small realised profit rather than a loss. Still, the decision was about more than the numbers.

First, the volatility never justified the returns. Second, and more fundamentally, the strategy never quite made sense. The folio mirrors publicly disclosed Renaissance Technologies 13F filings, reported with a long delay. Yet Renaissance's real edge always lived inside its Medallion Fund, which is famously closed to outside money and never publicly disclosed. In other words, you are copying the bits that leak out, not the engine that made the name. Jim Simons himself passed away in May 2024, so the folio never tracked him personally anyway. Given all that, I moved the proceeds into Pelosi+, which is why it is now my largest position.

What this Autopilot app review found over ten months

Point-in-time snapshots flatter copy trading. Therefore, the most useful thing I can share is the path, not a single number. The table below tracks my personal returns at each update, all before fees, with performance as at 21 June 2026.

| As at | Holding period | Pelosi+ | Jim Simons | Inverse Cramer | Blended |

|---|---|---|---|---|---|

| 9 Apr 2026 | ~8 months | +2.4% | -4.4% | +0.4% | -1.2% |

| 6 May 2026 | ~9 months | +18.3% | -1.2% | +12.0% | +9.7% |

| 21 Jun 2026 | ~10 months | +10.6%* | Sold at ~+1.5% | +26.6% | +11.9% |

*Pelosi+ now shows a blended +10.6% because it absorbed my Jim Simons money at a fresh cost basis. So this is not a like-for-like fall from May's +18.3% on the same cash.

Read across the rows and the story is clearly not a straight line up. The Inverse Cramer climbed steadily, from +0.4% to +12% to +26.6%. The Jim Simons folio, meanwhile, clawed back from -4.4% to a small profit before I exited. Pelosi+ soared and then settled once it took on the extra cash. Overall, my blended return moved from a small loss to +9.7%, and now to +11.9%. Past performance is not a reliable indicator of future results.

Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results. This is a personal account of my own experience, not financial advice. If you are unsure, consider speaking to a qualified financial adviser.

Thinking of trying it yourself?

You will need a connected Robinhood UK account first. Your capital is at risk, and returns like mine are in no way guaranteed.

Headline returns vs what I actually banked

Here is where copy trading gets slippery, and where this Autopilot app review earns its keep. When I last checked in early May 2026, the app's trailing 12-month folio figures looked staggering: Pelosi+ at +44.5%, the Jim Simons Tracker at +23.6% and the Inverse Cramer at +76.3%. Those are the numbers new users tend to see first.

However, I had only been invested for months, not a full year. My money also went in gradually, starting at $500 then drip-feeding monthly. As a result, my real returns landed nowhere near those banners. The Inverse Cramer's headline +76.3% became +26.6% in my account. Likewise, Pelosi+'s +44.5% translated into far less for me once timing and trade delays were factored in. So treat any copy-trading headline as marketing, not a forecast.

The volatility lesson

Copy trading does not move in straight lines, and my own figures prove it. Consider Pelosi+. On 9 April it sat at +2.4%; by 6 May it had leapt to +18.3%. Same app, same folio, wildly different snapshot in under a month. The Inverse Cramer, by contrast, kept grinding higher to +26.6%, though some of that owes to lucky timing on the quarterly rebalance rather than skill on my part.

For me, the takeaway is straightforward. If a single month can swing a position this much, then point-in-time performance means very little. What truly matters is whether you can stomach the journey. If you are weighing it up, my guide to investment risk for beginners is a sensible starting point before you copy anyone.

Is an automated, AI-led strategy any better?

Autopilot now offers AI-built and thematic folios alongside the politician and hedge-fund trackers. Naturally, that raises an obvious question: can an algorithm pick better than a congressperson? To find out, I have been running a separate, public experiment. You can follow how an AI-picked portfolio is actually doing week by week, with the same warts-and-all honesty as this Autopilot app review. Crucially, copying a folio, whether AI-led or politician-led, never guarantees similar returns. The FCA's InvestSmart hub is a sensible reality check before you start, because ultimately the decisions, and the risks, are yours.

The day trading trap

Because my Robinhood account is a margin account with under $25,000 in it, I am subject to the US Pattern Day Trader rule. That rule caps you at three day trades within a rolling five-business-day period. Over the ten months in this Autopilot app review, Autopilot triggered the restriction several times. The result was temporary freezes on my account. The first time, it looked like Autopilot was simply stuck, with trades sitting in limbo for days. Once you understand what is happening, it feels less alarming. Even so, it is a real friction point that Autopilot does not flag clearly enough.

Practical tips for UK users

After ten months of trial and error, here are the things I wish I had known from day one. First, always check your available balance in the Robinhood app rather than Autopilot, because the balance sync between the two can lag. Second, wait for one folio to finish trading before starting the next, so you avoid bottlenecks. Third, the stock blacklist feature is genuinely useful. My JPMorgan portfolio already exposes me to Tesla, so I blocked Tesla in Autopilot to avoid doubling up. Adding and removing stocks is easy.

The Autopilot app itself is well designed. The interface is clean, the folio breakdowns are detailed, and navigating between investments is intuitive. On the design front, it deserves real credit. The problem is not the app. Rather, it is the underlying complexity of running two apps side by side, plus the gap between marketed returns and what you actually experience month to month.

Value for money

The $99.99 annual fee is reasonable only if you invest enough to make it proportionally small. On my starting pot of $1,500, that was roughly 6.7% gone to fees in year one alone. That is steep. As I have added more each month, the effective percentage has dropped. Even so, it still needs factoring in. On top of that, you pay Robinhood's FX spread on every GBP deposit, plus whatever Wise charges for the subscription payment. Consequently, the all-in cost for a UK investor is higher than it first looks. If fees and FX matter to you, my breakdown of the cheapest investment apps and their FX fees is worth a read.

For comparison, my JPMorgan Personal Investing portfolio (risk level 10, sustainable ESG, held in a Stocks and Shares ISA) is up 22.82% after fees over the same roughly ten-month window. Over the past 12 months, it is up 26.68%. At my 6 May update, it was around 14.9% over its first nine months, so it has kept climbing. Crucially, those gains sit inside an ISA wrapper and are therefore tax-free. My Autopilot money, by contrast, sits in a standard Robinhood brokerage account with no ISA protection, so any gains there could face UK capital gains tax. Tax treatment depends on the individual circumstances of each client and may be subject to change in future.

One more thing matters here. My Autopilot figures are before the $99.99 subscription and Robinhood's FX costs, whereas the JPMorgan figure is already after fees. Strip Autopilot's costs out and the gap widens further. If you would rather invest tax-free, my roundup of the best investment ISAs for 2026 covers stronger options than a US brokerage. None of this is a recommendation; it is simply how the two have compared in my own accounts.

What about money you are not copy trading?

Copy trading is volatile by nature, so it is worth thinking about the other side of your finances too. For me, that means automating my mortgage. I have used Sprive with my Nationwide mortgage since October 2021, nudging small overpayments through in the background while Autopilot handles the riskier, optional pot. Naturally, the choice between investing and clearing debt is personal, and there is no universally right answer. If you are weighing it up, our look at whether to overpay your mortgage or invest sets out both sides. After all, a guaranteed return from overpaying carries no market risk, whereas a copy-trading folio carries plenty.

Investor protection: what UK users need to know

This point is easy to overlook. While Robinhood UK is regulated by the FCA (FRN: 823590), your securities and cash actually sit with Robinhood Securities LLC in the United States. As a result, your investments are protected by the US Securities Investor Protection Corporation (SIPC) up to $500,000, including $250,000 for cash. They are not protected by the UK's Financial Services Compensation Scheme. So the FSCS does not apply to your Robinhood brokerage holdings, and Autopilot, being US-based, sits outside that safety net entirely.

Robinhood has also bought additional insurance beyond SIPC, covering securities and cash up to $1 billion in aggregate, capped at $50 million per customer. That is reassuring, yet it remains a different framework from the one most UK investors know. By contrast, if you invest through a UK-based provider such as JPMorgan Personal Investing, eligible investments are protected up to £85,000 per person per FCA-authorised firm by the FSCS. Either way, none of these schemes cover losses from market movements. They only apply if the firm holding your assets fails.

Honest critical observations

Even with a healthy Inverse Cramer, I have plenty of genuine criticisms. First, the gap between Autopilot's headline numbers and what real users bank still feels misleading. New users see big trailing figures and assume they will get the same. As my own ten-month record shows, they rarely will.

Second, copying equity trades only is a fundamental limitation. The politicians and managers behind these folios often make their real money through options and derivatives. None of that is available to copy, so you get a watered-down version of the strategy. The Jim Simons folio was the clearest example, which is partly why I sold it.

Third, the "Pelosi" branding now feels stale. Nancy Pelosi has retired, so the folio is really a generic congressional tracker. Keeping her name on it flatters the marketing more than it informs investors. Finally, the volatility I keep seeing is not a feature; rather, it is a warning to anyone without the temperament to sit through the dips.

The verdict

Autopilot is a brilliant concept wrapped in a genuinely well-designed app. The idea of opening up the trading strategies of politicians and legendary investors is compelling, and the execution on the design front is slick. However, the reality for UK investors stays messier. You need two apps running in tandem, a Wise account for currency, and the patience to handle trade delays, notification overload, day-trading freezes and returns that can swing 10 to 20 points in a month.

In my experience, a properly managed, auto-balanced portfolio such as JPMorgan Personal Investing has simply worked better for me, especially inside an ISA. Even after a strong run on the Inverse Cramer, my JPM portfolio is comfortably ahead over the same window, with no monthly fiddling, no FX spreads and full ISA protection. For balance, FCA-regulated UK alternatives like Lightyear and Trading 212 are also worth a look if you want to invest without the dual-app gymnastics.

So, is Autopilot worth trying right now? Cautiously, at best. It is fun, educational and a great conversation starter. As a serious core strategy for UK investors, though, the friction, fees and volatility make it hard to justify. Many people who try copy trading keep it to a small slice of their portfolio rather than a core holding, but that is a personal call. Above all, do not expect either the headline numbers or this month's gains to be representative of what comes next.

Cool Factor

★★☆☆☆

2 out of 5

Overall, this Autopilot app review still lands at 2/5 Lukewarm. My numbers have improved since the spring, and the Inverse Cramer in particular has been a bright spot at +26.6%. Yet a quietly compounding ISA portfolio at JPMorgan has done better again over the same ten months, by a wider margin once Autopilot's fees are stripped out. Autopilot earns real credit for an innovative concept, a polished interface and a feature set few UK rivals offer. Even so, it falls short of Cool because real-world returns swing hard against the headlines, the dual-app setup adds avoidable friction for UK users, and the lack of ISA protection limits its usefulness as a core tool. It could be great one day. For now, though, one rough month would put it straight back in the red.

Frequently asked questions

Is the Autopilot app available in the UK?

Yes, but not directly. First, you open a Robinhood UK account and link it to the Autopilot app. Robinhood UK is FCA-regulated (FRN: 823590), although Autopilot itself is a US-registered investment adviser under the SEC. Your investments sit within Robinhood, not Autopilot.

Is Autopilot safe?

It depends what you mean by safe. On security, the setup is legitimate: Robinhood UK is FCA-authorised, and your assets sit with Robinhood Securities LLC in the US, protected by SIPC rather than the UK FSCS. On investment risk, though, no copy-trading folio is "safe". Capital is at risk, returns swing sharply, and past performance is not a reliable indicator of future results. So it is regulated and above board, yet far from low-risk.

How has Autopilot performed for me?

As at 21 June 2026, my personal returns (before fees) are: Inverse Cramer +26.6% and Pelosi+ +10.6% on a now-larger blended position. I also sold the Jim Simons Tracker at roughly +1.5%. Combined, my Autopilot pot is up around 11.9%. Just over two months earlier, on 6 May, it was up 9.7%, and back on 9 April it was down 1.2%. That swing is the best argument I can make for treating any single copy-trading figure with caution.

Is Autopilot better than an ISA or a cheaper app?

For me, not so far. Over the same roughly ten-month period, my JPMorgan Personal Investing portfolio inside an ISA is up 22.82% after fees, versus my Autopilot pot at 11.9% before fees. An ISA also shelters gains from tax, which a US brokerage does not. On cost specifically, several UK apps undercut the all-in price of running Autopilot; my cheapest investment app comparison breaks down the FX and fee differences. Autopilot is more fun and experimental, but it has not been the better investment for me.

Can you use Autopilot with an ISA?

No. Autopilot connects to your Robinhood brokerage account, and its copy trading does not work inside an ISA wrapper. As a result, any gains are potentially subject to UK capital gains tax. For tax-efficient investing, a Stocks and Shares ISA has worked better for me. Tax treatment depends on the individual circumstances of each client and may be subject to change in future.

Why are my Autopilot returns different from the reported folio performance?

Autopilot's reported returns reflect a folio's overall performance from a set start date, assuming a lump-sum investment. Your actual returns depend on when you invested, how much, and the trade delays involved. Pelosi+, for instance, runs around two weeks behind congressional filings. Dollar-cost averaging into a folio almost always means your results differ from the headline numbers.

Why is this Autopilot app review focused on UK investors?

Most existing Autopilot coverage is written for a US audience. As a result, it skips the bits that matter most to UK users: how to fund a Robinhood UK account, what the FX implications look like, how the FCA and SIPC protections compare, and whether any of it can sit inside an ISA. This Autopilot app review tries to fill that gap with real-world UK numbers.

Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results. This article is not financial advice. Performance, fees, rates and terms mentioned were accurate at the time of writing but can change at any time. Tax treatment depends on the individual circumstances of each client and may be subject to change in future. Consider speaking to a qualified financial adviser before making investment decisions. This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

More from CoolCuration

- Best investment referral deals UK - Compare the sign-up perks across the big UK investing apps before you pick one.

- Freetrade review UK - Another FCA-regulated, commission-free app worth weighing up as a Robinhood alternative.

- Lightyear referral - Our referral page for Lightyear, a UK-regulated app I also invest with.

- Stock Events app - A beautifully designed portfolio tracker that pairs nicely with Robinhood for watching dividends.

- Plum app referral - A UK-regulated, ISA-friendly alternative if you want auto-investing without the dual-app gymnastics.

What's trending

Recent posts

- Whistler Tate Britain Review: The Fullest Survey in 30 Years

Our Whistler Tate Britain review: nine rooms, the Nocturnes reunited and the etching room that invented the white cube. Budget for two visits, not one.

Our Whistler Tate Britain review: nine rooms, the Nocturnes reunited and the etching room that invented the white cube. Budget for two visits, not one. - Best Free Budgeting Apps UK 2026The best free budgeting apps in the UK for 2026, compared: what each free tier really includes, what is paywalled, and who each app suits.

- InvestEngine Review: My Honest Take After Six MonthsMy honest InvestEngine review after six months: no-fee ETF investing, the real bonus odds, and who this low-cost UK platform actually suits.

No Comments.