Last updated: 20 July 2026

By Stiv · Design, technology and personal finance

I have used Sprive with my Nationwide mortgage since October 2021, making regular overpayments through the app, so this is written from about four years of real use.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

This is not financial advice. It is one homeowner's experience, shared to help you make your own call.

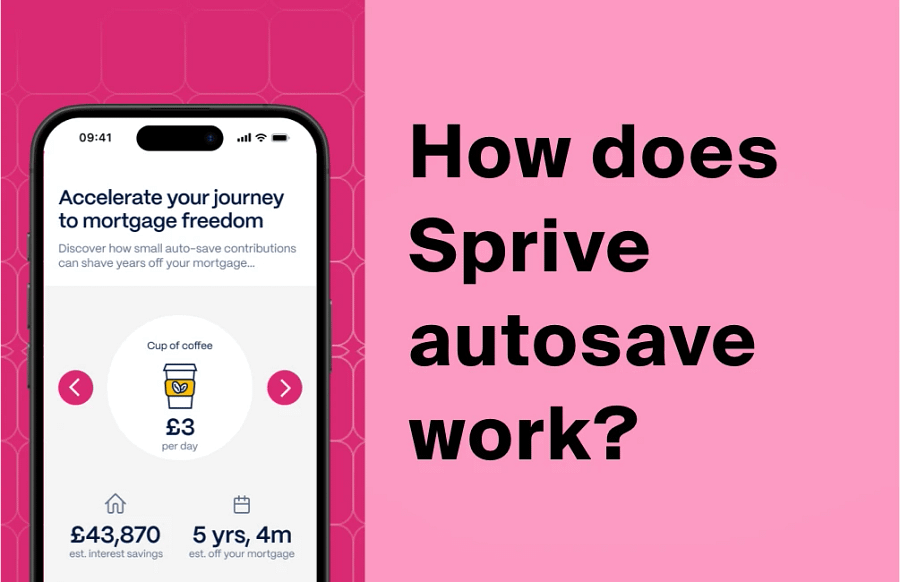

So you spotted the Sprive advert on the telly and wondered what that mortgage app actually is. Here is the short answer: yes, the mortgage app on the Channel 4 advert is Sprive, and it helps you chip away at your mortgage a little faster. Below, I explain what it does, whether it is legit, and what it is like after four years of real use.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Want to try the app from the advert?

The current Sprive sign-up offer and how to claim it are kept up to date on our referral page.

Read more