Last updated: 9 June 2026

By Stiv · Design, technology and personal finance

If you're still paying full price for your groceries, energy bills and online shopping in 2026, you're leaving hundreds of pounds on the table. The best cashback apps UK shoppers use have evolved far beyond basic reward schemes, with some offering instant payouts while others help you pay off your mortgage faster. We tested the UK's most popular cashback platforms to find out which ones actually deliver.

Whether you want passive earnings through card-linked tracking, instant supermarket discounts or mortgage overpayment bonuses, there's a cashback strategy that fits your spending habits. Here's everything you need to know about the best cashback apps UK shoppers are using in 2026.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view. This is information, not financial advice.

Our top cashback pick

If you only set one app up, TopCashback is the one I reach for first. It covers the most retailers and pays out from just £1.

How cashback apps actually work (and why retailers pay you)

Cashback apps earn commission when you shop through their platform or at partner retailers. Instead of pocketing the full amount, they share a portion with you as cashback. It's not complicated, and it's not a trick. Retailers pay for customer referrals the same way they pay for advertising. The difference is you get a cut instead of watching someone else profit from your spending.

There are three main types of cashback in 2026: affiliate-based platforms where you click through before shopping online (TopCashback, Quidco), card-linked apps that track automatically when you pay in-store or online (Airtime Rewards), and instant gift card cashback where you buy discounted vouchers before shopping (JamDoughnut, EverUp). Each has trade-offs between convenience, speed and earning potential.

TopCashback: the heavyweight for online purchases

TopCashback remains the UK's largest cashback site with over 6,000 retailers and typically the highest rates for online shopping. The platform works on an affiliate model. You search for a retailer on TopCashback, click through to their site and shop normally. Retailers pay TopCashback commission for sending customers their way, and TopCashback passes that commission back to you as cashback.

New-member bonuses vary through the year, with recent promotions offering around £10 to £20 after a qualifying spend. Check the current offer when you join, as the exact bonus and its end date change regularly.

Cashback rates depend on the retailer and product category. Insurance switches and broadband deals often pay £50 to £150 in cashback. Supermarkets and fashion retailers typically offer 1% to 4%, while electronics can reach 5% to 10% during promotional periods. The main drawback is the waiting time. Cashback takes 30 to 90 days to become payable because TopCashback needs the retailer to confirm your purchase wasn't returned.

TopCashback offers two membership tiers: a free Classic account and a Plus account. Plus costs £5 per year and gives you 5 to 16% higher cashback rates across participating retailers. If you shop online regularly, the Plus membership usually pays for itself within a few months, but the free tier works perfectly well for occasional users.

You can withdraw cashback via bank transfer, PayPal or convert it to gift vouchers with a bonus. The minimum payout threshold is just £1, making it easy to cash out whenever you want. For anyone making regular online purchases, TopCashback is one of the most useful to have.

Airtime Rewards: passive cashback on your phone bill

Airtime Rewards (now simply called Airtime) takes a completely different approach. Instead of clicking through links, you link your debit or credit cards to the app once and it automatically tracks purchases at partner retailers. Link your bank account to it and it automatically tracks your spending at 200+ retailers and usually gives you 1% to 15% cashback at them.

The cashback doesn't go into your bank account. It goes towards your mobile phone bill as credit. Once you've earned £10 of rewards, you can take it off your phone bill whether you're on Pay Monthly or Pay As You Go. For many people, this means a free month or two of phone service each year just for shopping normally.

Partner retailers include Boots, Argos, IKEA, Morrisons, Greggs, Waitrose and around 200 others. Cashback rates vary by retailer and sometimes by card type. You might see 5% at Brewdog if you have a Mastercard linked, but only 2% with a Visa. The app shows current rates for each retailer, so you always know what you'll earn before spending.

The major advantage is convenience. Once your cards are linked, you don't need to remember anything. You link your cards once, carry on shopping as normal, and your rewards build automatically in the background. The limitation is flexibility. You can only redeem rewards as phone credit, not cash. If your phone bill is £10 per month and you earn £3 monthly in cashback, that's useful. But you can't withdraw it to your bank account.

Airtime also introduced Airtime Up, an optional upgrade using Open Banking. With Airtime Up, you get faster redemptions at £5 instead of £10, faster rewards available in 1 day instead of up to 90, member-only retailers, and priority support. You'll need to renew Open Banking permissions every 90 days, which is standard security practice. Open Banking is regulated by the Financial Conduct Authority and uses secure, read-only access to your transaction data.

Airtime Rewards may suit you if you want effortless cashback with zero mental overhead, particularly if you shop regularly at Boots, Argos or major supermarkets.

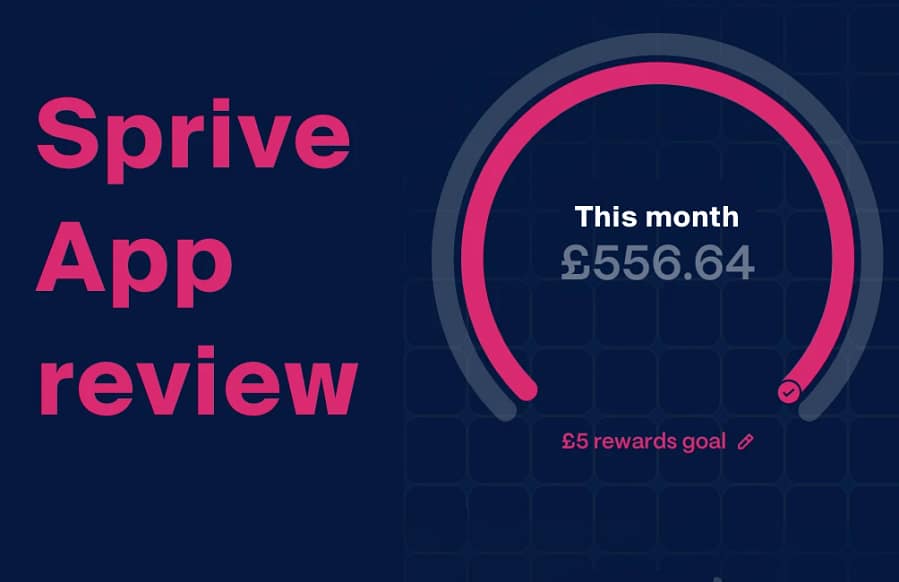

Sprive: cashback that pays off your mortgage

Sprive is different because it turns everyday shopping cashback into mortgage overpayments. The app helps homeowners make small, consistent overpayments to reduce their mortgage term and save interest. The cashback feature is the bonus that makes it easier to stick with.

You can earn cashback at UK brands like Amazon, M&S, Waitrose, ASDA, Morrisons, Tesco, Deliveroo and IKEA, which you can put towards paying off your mortgage. You buy digital gift cards through the Sprive app before shopping. For example, if you're doing a £100 weekly shop at Tesco, you buy a £100 Tesco gift card via Sprive first. You still spend £100 on groceries, but you might earn a few pounds cashback which Sprive credits to your account within 15 minutes.

That cashback goes directly towards mortgage overpayments. Sprive's own analysis suggests a one-off £5 cashback payment could reduce a mortgage balance by around £17.50 in interest over the term of a £250,000 mortgage at 5% over 30 years. The compound effect matters more than individual transactions, but overpaying is always subject to your lender's annual allowance.

The app also includes auto-saving features. You set minimum and maximum monthly limits, and Sprive automatically sets aside affordable amounts based on your spending patterns. When you're ready, it sends overpayments straight to your lender. Sprive supports many of the largest UK lenders and the minimum payment is £1.

The limitation is obvious: this only works if you have a mortgage and want to overpay it. You can't withdraw Sprive cashback as cash or use it for anything else. Sprive Limited is an appointed representative of Connect IFA Ltd (Sprive FRN 919863), and money in the Sprive wallet is safeguarded rather than FSCS-protected. Your home may be repossessed if you do not keep up repayments on your mortgage. If you're a homeowner focused on paying off your mortgage faster, see Sprive's referral offer and read our full Sprive app review for the complete breakdown.

Quidco: TopCashback's main rival

Quidco works almost identically to TopCashback with affiliate links for online shopping. The main differences are in specific retailer rates and Quidco's strength with utility switching deals. Quidco is the UK's second-largest cashback site with particularly strong offers for utility switching, insurance, and financial products.

If you're switching energy providers, comparing broadband deals or getting car insurance quotes, Quidco often has high cashback rates, sometimes £50 to £150 for a single switch. For everyday online shopping, rates are comparable to TopCashback, though one platform usually edges ahead depending on the specific retailer.

Quidco offers a free membership and a Premium tier. The Premium membership costs £1 per month and bumps up cashback rates across some retailers. Whether it's worth paying depends on how much you shop through the platform. For most people, the free version is perfectly adequate.

One practical approach is having both TopCashback and Quidco installed. Before any major online purchase, check both platforms and use whichever offers the better rate. It takes 10 seconds and often reveals a meaningful difference. Get started with Quidco or check our Octopus Energy guide to learn how to stack cashback with switching bonuses.

JamDoughnut and instant gift card cashback

JamDoughnut represents a different category of cashback app: instant gift card platforms. Instead of clicking through affiliate links and waiting months, you buy discounted gift cards through the app and earn cashback immediately. You buy gift cards for your favourite shops and earn cashback instantly from JamDoughnut.

The process is straightforward. If you're about to spend £100 at Sainsbury's, you buy a £100 Sainsbury's gift card from JamDoughnut first. You pay £100, but you might earn a few pounds cashback which appears in your account within minutes. You can then use that gift card to pay for your shopping in-store or online.

Typical rates range from 2% to 5% on supermarkets and major retailers. JamDoughnut is known for boosting cashback rates during pay weekends and special events. During these periods, you might see 5% cashback at Morrisons or other supermarkets, so it pays to watch for promotional periods.

The advantage over affiliate cashback is speed and reliability. There's no tracking to fail, no cookies to worry about, and no waiting months for confirmation. The cashback is instant. The limitation is that you need to remember to buy the gift card before shopping, though many users buy cards at the shop till, adding just a minute or two to the checkout process.

JamDoughnut may suit you if you want instant supermarket cashback without tracking headaches.

Stacking multiple cashback apps for maximum returns

Here's where cashback gets interesting: you can often use multiple apps on the same transaction. You may be able to stack the rewards with other cashback sites or apps to earn two separate amounts of cashback in a single transaction. For example, if you shop online via TopCashback or Quidco and pay with a card linked to Airtime, you'll theoretically get two lots of cashback.

This isn't guaranteed and depends on retailer terms, but it works surprisingly often. Some users report earning cashback from TopCashback for the online transaction, Airtime for paying with their linked card, and even their credit card's reward programme on top. That's three separate cashback streams on one purchase.

The key is understanding which apps work together. Card-linked apps like Airtime don't interfere with affiliate cashback because they track different aspects of the transaction. Gift card apps like JamDoughnut can sometimes stack with online cashback if the retailer allows it, though this requires more testing.

A realistic stacking strategy for 2026 looks like this: use TopCashback or Quidco for planned online purchases where rates justify the wait, set up Airtime to run automatically in the background for in-store shopping, and consider JamDoughnut or Sprive for weekly supermarket shops if you want instant cashback or mortgage benefits. Each layer adds value without much extra effort.

How much can you actually save with cashback apps?

Most UK households can realistically save £150 to £300 annually through cashback without changing spending habits. Based on £3,000 per year grocery shopping, a 4.3% rate saves you £129 per year. Add cashback from online purchases, energy switching and other categories, and £200 to £400 becomes achievable.

Heavy users who actively stack multiple platforms and watch for bonus offers report saving £500 to £1,000 annually. This requires more attention and discipline, checking cashback rates before every purchase and timing bigger spends around promotional periods. For most people, the sweet spot is using two or three apps consistently rather than trying to optimise everything.

The important thing is consistency. Installing the apps and using them occasionally won't move the needle. Making cashback a default part of your routine, where you automatically check before online purchases and use gift cards for weekly shops, compounds over time. A £200 annual saving might not sound dramatic, but over 10 years that's £2,000 plus any growth if you invest it.

Looking for more ways to stretch your money? Our guide to cutting household bills in the UK covers everything from energy switching to broadband deals.

Common cashback mistakes to avoid

The biggest mistake is making purchases just to earn cashback. If you buy something you don't need because it offers 10% back, you've still spent 90% you didn't need to spend. Cashback should enhance purchases you'd make anyway, not create new spending.

Another common error is not reading the cashback terms for affiliate platforms. Some retailers exclude certain product categories, discount codes or sale items from cashback. Always check the specific terms on TopCashback or Quidco before assuming a purchase qualifies. Nothing's more frustrating than waiting three months only to have a claim declined.

For card-linked apps like Airtime, the main pitfall is forgetting to unlock retailers. Some cashback partners appear "locked" in the app. If you don't manually unlock them before shopping, you won't earn anything even though the retailer seems available. Check the app before visiting shops to ensure everything's activated.

With gift card apps, the risk is buying cards for shops you don't actually visit. A 5% cashback rate looks great until you realise you never shop at that retailer and the gift card sits unused. Stick to places you genuinely frequent rather than chasing the highest percentage.

Finally, don't ignore payout minimums and expiry terms. Some platforms require minimum balances before withdrawal. Others mark accounts inactive if you don't use them for six months, potentially losing accrued rewards. Cash out regularly and keep accounts active even if it's just a small transaction every few months.

Which cashback app is best for you?

There isn't one single best cashback app because different tools serve different purposes. TopCashback suits online shopping variety and high-value transactions like insurance or holidays. Airtime Rewards suits people who want passive earnings with zero effort. Sprive suits homeowners serious about mortgage overpayments. Quidco suits utility switching deals. JamDoughnut suits instant supermarket cashback without tracking issues.

The practical approach is using multiple apps that complement each other rather than competing. A typical setup might include TopCashback for online purchases, Airtime running automatically in the background, and either Sprive or JamDoughnut for weekly food shopping depending on whether you have a mortgage. This covers most spending categories without overwhelming complexity.

Start with one or two apps, get comfortable with the routine, then add others if it makes sense for your spending. The best cashback strategy is the one you'll actually stick with. A simple system you use consistently beats a complex setup you abandon after two weeks.

Want to maximise your savings beyond cashback? Check out our roundup of the best referral offers in the UK and see how Sprive cashback actually works if you're considering the mortgage route.

Disclaimer: This article provides information only and is not financial advice. Cashback rates, terms and availability change frequently, so always verify current offers before signing up or making purchases. Your home may be repossessed if you do not keep up repayments on your mortgage. This page contains affiliate or referral links; if you sign up through one, we may earn a referral bonus at no extra cost to you, and it does not affect our editorial view.

Frequently asked questions about UK cashback apps

Are cashback apps actually safe to use?

Yes, established cashback platforms like TopCashback, Quidco, Airtime Rewards and Sprive are legitimate businesses that have operated for years. They make money by earning commission from retailers and sharing a portion with you. Gift card apps use Open Banking or secure payment integrations from FCA-regulated providers, though cashback apps themselves are not FCA-authorised financial products. Always stick to well-known platforms with proper reviews and avoid sketchy sites promising unrealistic returns.

How do cashback apps make money if they give me cash back?

Retailers pay cashback platforms a commission when you shop through them or use their referral links. The platform keeps a percentage and passes the rest to you as cashback. It's the same business model as affiliate marketing or price comparison sites. Everyone benefits: retailers get customers, platforms get commission, and you get money back on purchases you'd make anyway.

Can I use multiple cashback apps at the same time?

Yes, and you often should. Different apps cover different shopping scenarios. You can frequently stack card-linked cashback (like Airtime) with affiliate cashback (like TopCashback) on the same transaction because they track different things. Gift card apps sometimes stack with online cashback depending on retailer terms. The key is understanding which combinations work together.

How long does it take to receive cashback?

It depends on the app type. Gift card cashback apps like JamDoughnut and Sprive pay quickly once you buy the gift card. Card-linked apps like Airtime typically take a few days to confirm transactions. Affiliate platforms like TopCashback and Quidco take 30 to 90 days because they wait for retailers to confirm you didn't return items. Always check specific platform terms.

What's the minimum amount I can withdraw?

Most platforms have low minimums. TopCashback and Quidco typically allow withdrawals from £1. Airtime Rewards requires £10 of cashback (or £5 with Airtime Up) before you can apply it to your phone bill. Sprive has a £1 minimum for mortgage overpayments. JamDoughnut usually requires £10 before bank transfer. Check each app's specific terms as they can change.

Can cashback apps see all my bank transactions?

Only apps using Open Banking can see transactions, and they only see what's necessary for tracking cashback. They cannot move money without your explicit permission, and they don't see sensitive details like your login credentials. Card-linked apps like Airtime only see transactions at partner retailers, not your full spending history. Traditional affiliate sites like TopCashback use browser cookies and don't access your bank at all. For more guidance on cashback safety, Money Saving Expert provides comprehensive consumer advice on cashback platforms.

Do I still get cashback if I use a discount code?

Usually yes, but not always. Most retailers allow you to stack cashback with discount codes, but some exclude promotional purchases or specific voucher types from cashback eligibility. Always read the specific terms on the cashback platform before making a purchase. If a deal seems too good, check whether it qualifies for cashback before assuming it will track.

What happens if my cashback doesn't track?

Most platforms offer a claims process if cashback fails to track. You'll typically need proof of purchase like an order confirmation email or receipt. TopCashback and Quidco have specific claim forms with varying success rates. Card-linked apps like Airtime and gift card platforms rarely have tracking issues because the cashback is tied directly to the payment method or gift card purchase rather than browser cookies.

Is it worth paying for premium cashback memberships?

It depends on your spending volume. TopCashback Plus costs £5 yearly and increases rates by 5% to 16%. If you shop online frequently, it pays for itself quickly. Quidco Premium costs £1 monthly and offers similar benefits. Calculate whether the extra cashback from your typical spending exceeds the membership fee. For light users, free tiers work perfectly well. For heavy users, premium tiers usually make financial sense.

Can I use cashback apps for business purchases?

Most cashback platforms are designed for personal use and prohibit business transactions in their terms. Using cashback apps for business purchases could result in account suspension or cashback being declined. If you're self-employed or run a small business, check platform terms carefully or contact support before assuming business spending qualifies.

Related articles you might find useful

- Best SIM-only deals UK 2026: stack cashback with the cheapest mobile contracts around.

- Honest Mobile referral code: ethical mobile network with cashback opportunities.

- Sentia alcohol-free spirits: a great gift for mindful drinkers.

- Gift guide for foodies: thoughtful presents for food lovers.

- Is Octopus Energy regulated by Ofgem?: everything about Octopus's regulatory status.

What's trending

Recent posts

- The Odyssey IMAX 70mm Review: Worth It at BFI Waterloo?

Nolan's Odyssey on a 15-perf celluloid print at BFI Waterloo. Overwhelming craft, a career-best Matt Damon, one unforgettable Circe scene, two castings that do not work and a sound mix that buries the dialogue. Cool Factor: 4/5. #TheOdyssey #IMAX70mm #ChristopherNolan #FilmReview #BFIIMAX

Nolan's Odyssey on a 15-perf celluloid print at BFI Waterloo. Overwhelming craft, a career-best Matt Damon, one unforgettable Circe scene, two castings that do not work and a sound mix that buries the dialogue. Cool Factor: 4/5. #TheOdyssey #IMAX70mm #ChristopherNolan #FilmReview #BFIIMAX - Dyson HushJet vs Sans Mini: Air Purifier ReviewWe bought both compact purifiers so you don't have to. One costs £150 more, skips HEPA and locks you into an app rated 3.8 out of 5. Full honest verdict inside. #airpurifier #dyson #sansair #hometech #ukhome

- Best Audiobooks August 2026: 10 UK Listens Worth a CreditSorted your August listening? Our best audiobooks of August 2026 are in: Toni Collette as Miss Marple, Rachel Cusk narrating her own novel, Robert Harris in ancient Rome and a grave-robbing horror comedy. Tap through for runtimes, prices and where to listen. #audiobooks #Audible #WhatToRead #AugustReads #BookTok

No Comments.