Last updated: 9 June 2026

By Stiv · Design, technology and personal finance

Over 24 million people in the UK hold Premium Bonds, which makes them the nation's most popular savings product. Yet most holders have never weighed up Chip Prize Saver vs Premium Bonds side by side, and the numbers reward a closer look. Around 62% of Premium Bonds holders have never won a single prize, according to AJ Bell. The prize fund rate sits at 3.30% for the June 2026 draw, with each £1 bond facing odds of 23,000 to 1. From the July 2026 draw, however, NS&I lifts the rate to 3.80% and shortens those odds to 22,000 to 1.

Meanwhile, Chip's Prize Savings Account offers an alternative: a prize-draw savings account that claims roughly 3.5 times better odds than Premium Bonds, plus quarterly big prizes reaching £250,000. We are not saying Premium Bonds are bad. Indeed, they are backed by the Treasury and pay tax-free prizes, which is a real advantage. However, if you have not compared them to anything in years, this is worth ten minutes of your time.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

Want to try the Chip Prize Saver?

Our Chip referral page carries the current new-customer bonus and the sign-up steps, kept up to date.

This article is for informational purposes only and does not constitute financial advice. It is not a recommendation to open, close, or switch any savings or investment product. Always do your own research or consider a qualified financial adviser before making financial decisions. CoolCuration is not authorised by the Financial Conduct Authority. Tax treatment depends on individual circumstances and may change. All product details were verified at the time of writing but may change, so always check the provider's website for current terms.

How Premium Bonds work

Premium Bonds are a savings product from National Savings and Investments (NS&I), which is backed by HM Treasury. Instead of earning interest, each £1 you put in buys a bond that enters a monthly prize draw. Prizes range from £25 up to £1 million, and two people win the £1 million jackpot every single month.

Winners are picked by ERNIE (Electronic Random Number Indicator Equipment), which generates random numbers each month. All Premium Bonds prizes are free of UK Income Tax and Capital Gains Tax, according to NS&I. Moreover, you can buy bonds from £25 up to a maximum holding of £50,000 per person, and anyone aged 16 or over can hold them. New bonds must sit for one full calendar month before they qualify for the draw.

Here is the bit that catches people out: the prize fund rate is not an interest rate. It currently sits at 3.30% for the June 2026 draw, then rises to 3.80% from the July 2026 draw, according to NS&I's official announcements. This variable rate sets the size of the total prize pool. It reflects what someone with perfectly average luck might receive over time. In reality, most individual holders receive far less, and many receive nothing at all.

How Chip Prize Saver works

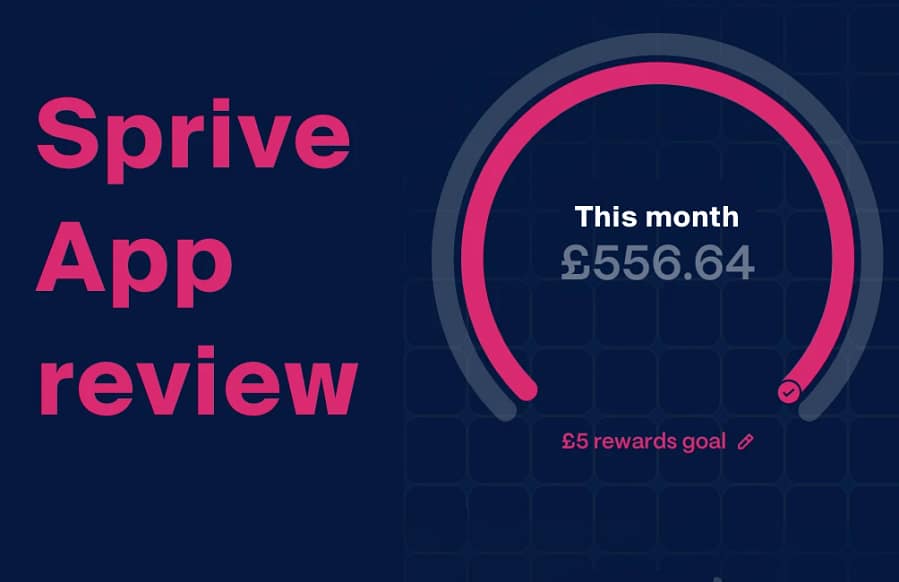

The Chip Prize Savings Account is a savings product inside the Chip app. Like Premium Bonds, it pays no interest (0% AER). Instead of interest, your balance earns entries into a monthly prize draw. Specifically, Chip enters you into the draw if your average monthly balance is at least £100, and you receive one entry for every full £10 of average balance.

Chip Financial Ltd is authorised and regulated by the Financial Conduct Authority (FCA reference 911255). The account itself is provided by ClearBank, a UK-authorised bank (FCA reference 754568). Therefore your money sits with a regulated deposit-taker rather than with Chip directly. You can hold up to £85,000, withdrawals are near-instant, and there are no fees for holding the account or entering the draw.

Prize amounts change from month to month. For the standard April 2026 draw, Chip offered one grand prize of £10,000, plus 7 prizes of £500, 73 prizes of £100, 180 prizes of £20, 360 prizes of £10, and 14,400 prizes of £5, a total pool of around £100,000. Every quarter, Chip runs a bigger draw. In March 2026, for instance, the grand prize reached £250,000 alongside 100 prizes of £1,000 and thousands of smaller £5 and £10 wins, for a £500,000 pool.

Chip Prize Saver vs Premium Bonds: at a glance

| Feature | Premium Bonds | Chip Prize Saver |

|---|---|---|

| Provider | NS&I (HM Treasury) | Chip, deposits held by ClearBank |

| Interest (AER) | None (prize draw only) | None, 0% AER (prize draw only) |

| Prize rate | 3.30% June 2026, 3.80% from July (variable) | No fixed rate published |

| Draw frequency | Monthly | Monthly, with a quarterly big draw |

| Top prize | £1,000,000 (two per month) | £10,000 monthly / £250,000 quarterly |

| Smallest prize | £25 | £5 |

| Tax on winnings | Tax-free | Tax-free (per Chip's terms) |

| Protection | 100% HM Treasury backed | FSCS up to £120,000 via ClearBank |

| Minimum | £25 | £100 average balance to qualify |

| Maximum | £50,000 | £85,000 |

| Withdrawal speed | Usually within 3 banking days | Near-instant |

| Entry calculation | 1 entry per £1 held | 1 entry per £10 average balance |

Both products work on the same principle: you save money, earn no interest, and instead enter a prize draw. As a result, the comparison comes down to the odds, the prize sizes, how your money is protected, and which structure fits your circumstances.

The odds of winning compared

This is where the match-up gets interesting, and where the numbers need care.

For Premium Bonds, NS&I sets the odds of each £1 bond winning any prize at 23,000 to 1 for the June 2026 draw, shortening to 22,000 to 1 from July. So if you hold £1,000, you have 1,000 entries each month, which gives you roughly a 4.3% chance of winning at least one prize that month. Over a year, you might expect one or two small wins, and most would be £25.

For Chip, the picture is harder to pin down because Chip publishes no fixed prize rate. However, the figures Chip reported for 2025 put the odds of winning anything at roughly 1 in 900 to 1 in 1,000 for every £10 of average balance, with a stronger 1 in 623 in its September 2025 draw. On that basis, Chip claims its odds are about 3.5 times better than Premium Bonds. The trade-off is clear: shorter odds, but much smaller top prizes.

| Odds factor | Premium Bonds | Chip Prize Saver |

|---|---|---|

| Odds of any prize | 23,000 to 1 per £1 (22,000 to 1 from July) | Around 1 in 900 to 1 in 1,000 per £10 (variable) |

| Entries | 1 per £1 held | 1 per £10 average balance |

| Published prize rate | Yes (3.30%, rising to 3.80%) | No |

| Most common prize | £25 or £50 (around 84% of prizes) | £5 |

Prize amounts and tiers

The prize ladders look very different. Premium Bonds run from £25 at the bottom to two £1 million jackpots at the top, with bands at £50, £100, £500, £1,000, £5,000, £10,000, £25,000, £50,000 and £100,000 in between. That said, around 84% of all prizes are £25 or £50, so the headline jackpots are vanishingly rare.

Chip's ladder is shorter and lands lower. In a standard month the top prize is £10,000, with bands at £5, £10, £20, £100 and £500 below it. Each quarter, the big draw lifts the top prize to £250,000. Consequently, Chip pays out more frequent small wins, whereas Premium Bonds dangle the life-changing jackpot that almost nobody hits.

Realistic returns: what the maths really shows

The prize fund rate is an average, not a promise. NS&I builds a pool equal to 3.30% of all money in Premium Bonds (3.80% from July), then shares it out. Because the jackpots and bigger prizes swallow a chunk of that pool, the typical holder receives less than the headline rate. For many savers, the median return in a given month is simply zero.

A worked example helps. With average luck, £10,000 in Premium Bonds might win around £250 a year at the 3.30% rate, rising to roughly £300 once the rate moves to 3.80%. A smaller £1,000 holding might win nothing in most years, bar the occasional £25. Indeed, AJ Bell found that 62% of all holders have never won, and that the average balance among never-winners is just £128.91.

Chip pays out more often, but in smaller amounts. With £1,000 you hold around 100 entries, so a small £5 win is more likely month to month. Over a year, though, the running total stays modest, and Chip gives you no rate to forecast it with.

For comparison, a normal easy-access account paying around 4.5% AER (variable) would hand £10,000 roughly £450 over a year, with no luck involved. So if steady, predictable growth matters more than the thrill of a draw, a standard savings account or cash ISA is likely to leave you better off. Our best savings account UK guide tracks the current top rates, and MoneyHelper has impartial guidance on saving.

Speed of withdrawals

Chip wins clearly on access. You can withdraw from the Prize Savings Account through the app, and the money usually lands in your linked bank account near-instantly. One quirk is worth knowing: any prizes you win sit as a bonus balance, and they only become spendable cash once you withdraw your full balance and pay it back in.

Premium Bonds are slower. You can cash in online, in the app, by phone or by post, with no notice and no penalty. However, NS&I aims to return the funds within three banking days, so it is not the place for money you might need the same day.

Safety and protection: Treasury backing vs FSCS

Both products keep your capital safe, but through different routes, and the distinction matters.

Premium Bonds are backed 100% by HM Treasury. That is a government guarantee on your full holding, up to the £50,000 cap, so the usual FSCS limit does not apply. Your capital cannot fall in value.

Chip's Prize Savings Account works differently. Your money is held by ClearBank, a UK-authorised bank. Eligible deposits are protected up to £120,000 per eligible person per UK-authorised bank, building society or credit union by the FSCS (since 1 December 2025). Because ClearBank also holds Chip's other accounts, that £120,000 covers your Cash ISA, Instant Access, Easy Access Saver and Prize Savings balances combined, rather than each one separately. You can confirm the detail on the FSCS website.

Neither product can lose your capital. Both, however, can lose purchasing power. If you win nothing, inflation quietly erodes the real value of money that earns no interest.

Limits and eligibility

Premium Bonds are open to anyone aged 16 or over, and adults can also buy them for under-16s. You can hold from £25 up to £50,000, and new bonds enter the draw after one full calendar month. Chip's Prize Savings Account is open to Chip customers who are UK residents aged 18 or over. You need an average balance of at least £100 to be entered, and you can hold up to £85,000. So if you have already maxed out Premium Bonds, Chip gives you extra headroom for prize-draw saving.

Who each one suits

Neither product is objectively better, and the right answer depends on your circumstances.

Premium Bonds may suit you if you hold a large lump sum, value rock-solid Treasury backing above all else, or are a higher-rate taxpayer who has used up the Personal Savings Allowance and wants tax-free saving with a shot at a big jackpot.

Chip Prize Saver may suit you if you like an app-based experience, want near-instant access, prefer shorter odds and more frequent small wins, or want prize-draw headroom beyond the £50,000 Premium Bonds cap.

Neither may suit you if your priority is predictable growth. Since both pay no interest, a standard savings account or cash ISA would give you a predictable return instead of relying on luck. If you are weighing up spare cash more broadly, our guide on whether to overpay your mortgage or invest is worth a read.

Where each one falls short

Premium Bonds have real weaknesses. The prize fund rate flatters the typical experience, the odds are long for smaller holders, withdrawals take a few days, and 62% of holders have never won a penny. The £50,000 cap also limits how much you can park there.

Chip Prize Saver has its own gaps. It publishes no fixed prize rate, so you cannot forecast returns the way you can with Premium Bonds. The top prizes are far smaller, the prize structure shifts every month, and the prize-to-cash withdrawal quirk adds friction. Crucially, neither product pays interest, so both can underperform a plain savings account over time.

Can you use both?

Yes, and plenty of people do. There is nothing stopping you splitting savings across both. Some keep Premium Bonds for the tax-free jackpot chance and Treasury backing, while using Chip for the app experience and more frequent smaller wins. If you already hold the maximum £50,000 in Premium Bonds, Chip's £85,000 cap gives you extra room. Just remember that money in either product earns no interest, so weigh it against what you could earn in a standard savings or investment account.

This article is for informational purposes only and does not constitute financial advice. It is not a recommendation to open, close, or switch any savings or investment product. Always do your own research or consider a qualified financial adviser before making financial decisions. CoolCuration is not authorised by the Financial Conduct Authority. Tax treatment depends on individual circumstances and may change. Prize rates are variable. All product details were verified at the time of writing but may change, so always check the provider's website for current terms.

Frequently asked questions

What are the odds of winning Premium Bonds?

For the June 2026 draw, the odds of each £1 bond winning any prize are 23,000 to 1, according to NS&I. From the July 2026 draw, those odds shorten to 22,000 to 1 as the prize rate rises to 3.80%. To put that in context, £1,000 of bonds gives you 1,000 entries and roughly a 4.3% chance of a prize in any month. With the maximum £50,000 your odds improve, yet AJ Bell research found that 62% of all holders have still never won anything.

Is Chip Prize Saver better than Premium Bonds?

It depends on what you value. Chip claims roughly 3.5 times better odds per entry, offers near-instant withdrawals, and allows a higher balance (£85,000 versus £50,000). However, Premium Bonds offer far larger top prizes (two £1 million jackpots a month), clear tax-free status, a published prize rate, and 100% HM Treasury backing. Neither pays interest, so for predictable returns a standard savings account would beat both.

How long do Premium Bonds take to withdraw?

You can cash in Premium Bonds online, in the NS&I app, by phone or by post, with no notice and no penalty. NS&I aims to return the money to your bank account within three banking days. By contrast, Chip Prize Saver withdrawals are usually near-instant through the app, so Chip is the better option if same-day access matters.

Are Premium Bonds worth it?

They can be, in the right hands. Premium Bonds suit people who value Treasury-backed security, want tax-free saving, and have a large enough holding to win with some regularity. For smaller balances, the long odds mean most people win little or nothing, so a high-interest savings account is likely to deliver more. The rate rising to 3.80% in July 2026 narrows the gap, but the return is still down to luck.

What is the Chip Prize Saver interest rate?

The Chip Prize Savings Account pays no interest (0% AER). It is a non-interest-bearing account, much like Premium Bonds, where your balance buys entries into a monthly prize draw instead of earning a rate. If you want to earn interest with Chip, its separate Instant Access Account, Easy Access Saver and Cash ISA do pay interest. Those are different products from the Prize Savings Account.

Is Chip Prize Savings safe?

Yes. The account is provided by ClearBank, a UK-authorised bank regulated by the FCA and PRA. Eligible deposits are protected up to £120,000 per eligible person per UK-authorised bank by the FSCS (since 1 December 2025). That limit applies across all your ClearBank balances held through Chip combined, including any Cash ISA, Easy Access Saver or Instant Access Account, rather than to each account separately.

Can you lose money in Premium Bonds or Chip Prize Saver?

You cannot lose your capital with either product, within the protection limits described above. Premium Bonds are backed by HM Treasury, and Chip deposits are FSCS protected via ClearBank. However, both can lose purchasing power. If you win nothing, your money earns no interest, so inflation reduces its real value over time. That is the genuine risk with any prize-draw saving.

What is the average Premium Bonds return?

The prize fund rate is the average, currently 3.30% and rising to 3.80% in July 2026. That figure is a mean across all holders, not what a typical saver receives. Because the jackpots and larger prizes skew the average, most holders earn less, and the median return is often zero in a given month. With average luck, £10,000 might win around £250 to £300 a year, while smaller holdings frequently win nothing.

More from CoolCuration

- Chip app guide: everything you need to know about saving and investing with Chip.

- Monzo referral: a current bank-account bonus, a random £5 to £50, you can claim alongside your savings.

- Best savings options for the new tax year: where to put your money now the ISA allowance has reset.

- Gifts under £25: thoughtful finds that prove you do not need to spend big.

- Oura Ring 4: the smart ring that tracks your sleep, recovery and daily readiness.

What's trending

Recent posts

- Best Refurbished iPads UK 2026: Which One to Buy

The best refurbished iPads to buy in the UK in 2026, ranked by who they suit, with Back Market and Amazon Renewed compared so you can pick the cheapest route.

The best refurbished iPads to buy in the UK in 2026, ranked by who they suit, with Back Market and Amazon Renewed compared so you can pick the cheapest route. - Summer Exhibition 2026 review: Ryan Gander opens up the RALast updated: 17 June 2026 By Tristan · Arts, exhibitions and creative culture Royal AcademySummer Exhibition 2026 Less fuss, more finds: Gander opens up the RA I went in slightly braced to this year's Summer Exhibition 2026, because the world's biggest open-submission show can be exhausting, but I came out cheerful. Ryan Gander's turn as… Read more: Summer Exhibition 2026 review: Ryan Gander opens up the RA

- Best Back Market Deals UK: June 2026 PicksLast updated: 28 June 2026 By Stiv · Design, technology and personal finance This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view. Refurbished techJune 2026 edit The Back Market… Read more: Best Back Market Deals UK: June 2026 Picks

No Comments.