Last updated: 21 June 2026

By Stiv · Design, technology and personal finance

Finding the best investment ISA in 2026 really comes down to one question: what kind of investor are you? So instead of crowning a single winner, this guide matches the main UK stocks and shares ISA platforms to the people they actually suit, then compares them on the things that move the needle: fees, FX costs, choice of investments and how easy each one is to use.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

Not financial advice. This article is for information only and reflects personal experience, not a recommendation. Because investing carries risk, always do your own research or speak to a qualified financial adviser before you act.

Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results.

The low-cost ISA we track most

For transparency, Lightyear is the low-cost Stocks and Shares ISA we use and follow most closely, so you will see it referenced throughout. It is also the account behind our living can AI turn £1,000 into £10,000 experiment. You can check its current ISA details and any live offer on our referral page before you decide anything.

Section 01 / The essentials

First, the ISA rules for 2026/27

Before the platforms, here is the bit that decides how much you can actually shelter this year.

The ISA allowance for the 2026/27 tax year is £20,000, and the government confirms that figure on its official ISA guidance. Crucially, it does not roll over. So if you do not use this year's allowance, you lose it for good when the tax year ends.

You can also split that £20,000 across different ISA types in the same year. For example, you might hold a cash ISA, a stocks and shares ISA and a Lifetime ISA (up to £4,000) at once, as long as your total stays within the limit. Moreover, since April 2024 you can pay into more than one ISA of the same type in a single tax year, and partial transfers are allowed too. The Lifetime ISA remains the exception, because you can still only pay into one per year.

Key dates: the tax year runs from 6 April 2026 to 5 April 2027. Therefore, your deadline to use this year's allowance is midnight on 5 April 2027.

Stocks and shares ISA vs cash ISA

Next, the question almost everyone asks. A cash ISA pays interest and your balance does not fall, so it suits money you might need within the next few years. A stocks and shares ISA, by contrast, invests in things like funds, ETFs and individual shares, so it has more growth potential over the long run. However, its value can also drop, sometimes sharply.

In short, the steer is about time. For short-term savings, cash usually wins on safety. For goals five years away or more, a stocks and shares ISA is worth weighing up. Inside that wrapper you pay no capital gains tax and no dividend tax, and you do not declare ISA gains on a tax return. Because the capital gains tax allowance is now just £3,000 for 2026/27, that shelter matters more than it used to. If you are still finding your feet, our beginner's guide to investment risk and our how to start investing guide are useful next reads.

Tax treatment depends on the individual circumstances of each client and may be subject to change in future.

Section 02 / The picks

Best investment ISA picks for 2026

Seven platforms, sorted by the kind of investor each one fits, from low-cost DIY apps to a fully managed pot.

Of course, there is no single best investment ISA for everyone. So the right pick depends on whether you want to choose your own investments or hand that job over, how much you plan to invest, and which fees you are happy to pay. With that in mind, here is how the main options compare.

Not advice, and capital at risk. The platform links below are referral links. This is information based on personal use, not a recommendation, so always check the provider's current terms first.

Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results.

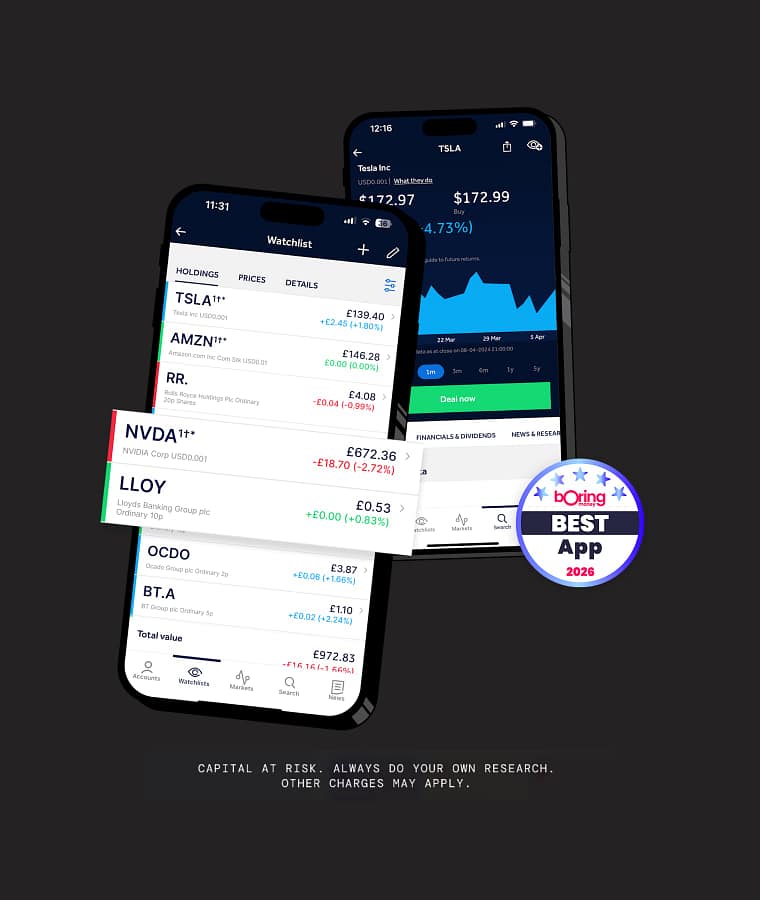

Trading 212

Trading 212 gives you a free stocks and shares ISA with no platform fee and no dealing commission. Its FX fee is a low 0.15%, and its Pies feature lets you build auto-investing baskets that rebalance for you. As a result, it works for hands-on and hands-off styles alike.

That said, the huge choice can overwhelm a brand-new investor, and the FX fee still applies on overseas shares. Trading 212 UK Limited is authorised and regulated by the Financial Conduct Authority (FRN 609146).

for the investor who wants one app to do it all

Free ISA, 0.15% FX

Freetrade

Freetrade now includes its stocks and shares ISA, Junior ISA and SIPP for free on the Basic plan, which is a genuine shift from 2025. So you can run an ISA and a pension from one app at no monthly cost. Paid plans (Standard from £4.99 a month, Plus from £9.99 a month billed annually) cut the FX fee and add interest on cash.

Freetrade also runs a refer-a-friend offer where you and a friend each get a free share worth between £10 and £100. However, most awards sit at the lower end, the share is picked from a pool, capital is still at risk and terms apply. The FX fee on Basic is also high at 0.99%, so frequent US buyers may prefer a paid tier. Freetrade Limited is authorised and regulated by the Financial Conduct Authority (FRN 783189). For more, read our Freetrade review.

for the investor who wants an ISA and a pension in one place

Free Basic plan, free SIPP

Lightyear

Lightyear is the low-cost ISA we track most, and its numbers explain why. Specifically, there is no platform fee, no dealing commission and an FX fee of just 0.10%. On top of that, it gives access to more than 6,000 shares, ETFs and money market funds across UK, US and EU markets, with multi-currency GBP, USD and EUR accounts so you can avoid repeat conversions.

It also pays interest on uninvested cash and runs a separate cash ISA. However, money in Vaults sits in money market funds rather than a bank, so it is not FSCS-protected as deposits and the rate is variable. In other words, treat that as investing, not saving. Lightyear U.K. Ltd is authorised and regulated by the Financial Conduct Authority (FRN 987226), and eligible investments are protected up to £85,000 per person per FCA-authorised firm by the FSCS. For the full picture, see our Lightyear review.

On a personal note, it is also the account we use for our weekly can AI turn £1,000 into £10,000 experiment, where we track AI-picked shares inside a real Lightyear portfolio.

for the investor chasing low costs on global shares

Free ISA, 0.10% FX

InvestEngine

InvestEngine takes a different route. Its DIY ISA charges 0% in platform fees, no dealing commission and no FX fee, so the main cost is the ETF's own ongoing charge, which starts from around 0.03%. For hands-off savers, its ready-made LifePlan portfolios do the picking for you.

The trade-off is range. You can only buy ETFs here, not individual shares, and its standalone managed portfolios are currently closed to new clients. You can also check its full charges on the InvestEngine costs page. InvestEngine (UK) Limited is authorised and regulated by the Financial Conduct Authority (FRN 801128).

for the investor happy to build a portfolio from ETFs

0% platform fee, no FX fee

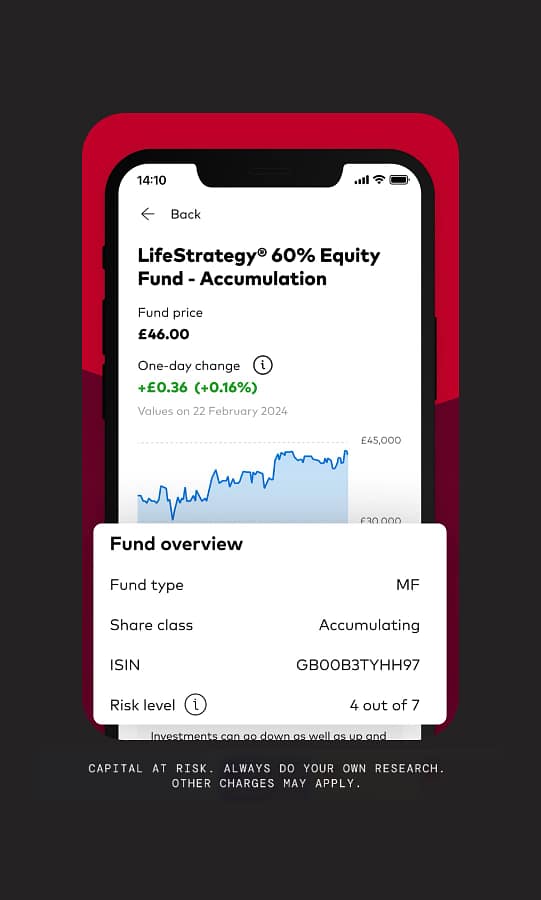

Vanguard Investor

Vanguard Investor is, above all, the home of low-cost index funds, including the popular LifeStrategy range. Its account fee is 0.15% a year, capped at £375, which is excellent value on a large pot. You can open an ISA from £500 as a lump sum or £100 a month.

There are two catches, though. First, a £4 monthly minimum fee (£48 a year) now applies to self-managed accounts under £32,000, so smaller pots pay more in percentage terms. Second, you can only buy Vanguard's own funds, not shares from elsewhere. Vanguard Asset Management, Ltd. is authorised and regulated by the Financial Conduct Authority (FRN 527839).

for the long-term investor who loves cheap index funds

0.15% a year, £375 cap

No single platform wins. The best investment ISA is simply the one that fits how you invest.

Hargreaves Lansdown

Hargreaves Lansdown is, by contrast, the heavyweight, with deep research, a vast investment range and strong customer service. Helpfully, it cut its ISA fund charge from 0.45% to 0.35% on 1 March 2026, and share dealing dropped to £6.95. So it is more competitive than it was, especially for fund investors.

Even so, it is pricier than the app-based platforms above, fund dealing now costs £1.95 a trade, and the share-holding cap inside the ISA rose to £150 a year. Hargreaves Lansdown Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FRN 115248).

for the investor who wants research, scale and support

0.35% on funds, capped for shares

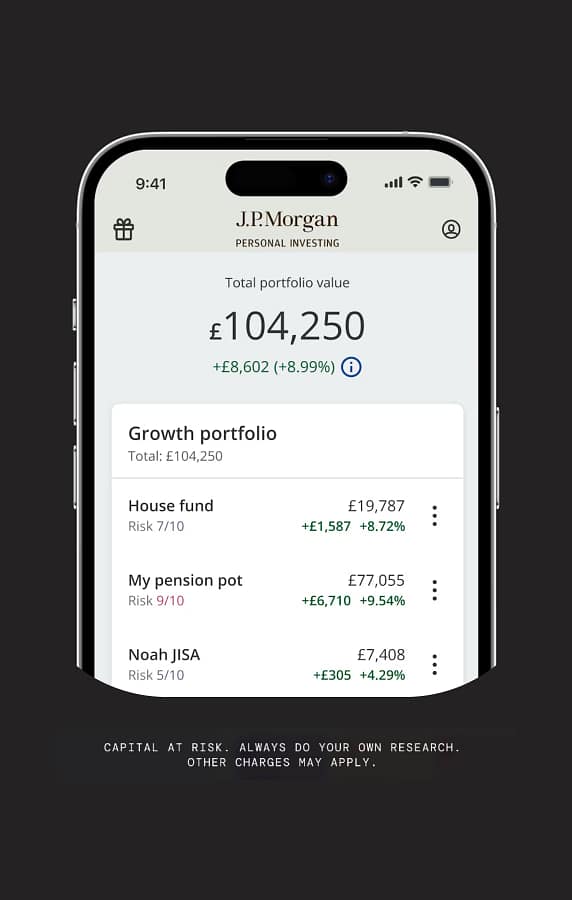

J.P. Morgan Personal Investing

J.P. Morgan Personal Investing (formerly Nutmeg) does the investing for you. In short, you pick a risk level and a style, then its team builds and manages the portfolio. Fees start at 0.45% a year on the first £100,000 for Fixed Allocation and 0.75% for fully managed, with underlying fund costs on top. Naturally, that buys convenience rather than the lowest price.

For new customers, J.P. Morgan regularly runs an introductory offer, currently 6 months with no J.P. Morgan management fees via the link on our referral page. Underlying fund charges still apply during that period, and because terms change we keep the latest offer on that page, so check it first. Still, the cost is higher than DIY, and you give up control over individual holdings. J.P. Morgan Personal Investing Limited is authorised and regulated by the Financial Conduct Authority (FRN 552016), and eligible investments are protected up to £85,000 per person per FCA-authorised firm by the FSCS. Capital at risk. Terms apply.

for the investor who would rather not pick anything

From 0.45% a year, managed

Tax treatment depends on the individual circumstances of each client and may be subject to change in future.

Quick comparison: best investment ISA 2026

| Platform | ISA platform fee | FX fee | Investments | Best for |

|---|---|---|---|---|

| Trading 212 | Free | 0.15% | 12,000+ shares and ETFs | All-round DIY |

| Freetrade | Free (Basic) | 0.99% Basic to 0.39% Plus | 6,500+ shares and ETFs | ISA plus free SIPP |

| Lightyear | Free | 0.10% | 6,000+ shares, ETFs and MMFs | Low FX, global |

| InvestEngine | 0% (DIY) | None | 700+ ETFs only | ETF-only investors |

| Vanguard Investor | 0.15% (£4/mo min, £375 cap) | Not applicable | About 85 Vanguard funds | Index-fund fans |

| Hargreaves Lansdown | 0.35% on funds (capped) | 0.99% tiered | Thousands of funds, shares, trusts | Full service |

| J.P. Morgan | From 0.45%/yr managed | Not applicable | Ready-made managed portfolios | Hands-off |

Remember that a headline "free" platform still has costs, most often the FX fee on overseas shares plus each fund's own ongoing charge. So compare the total, not just the sticker. For a deeper look at hidden currency costs, see our guide to the cheapest investment app and FX fees compared. And to weigh up sign-up bonuses, our best investment referral deals roundup keeps track of the latest offers.

Which ISA has the lowest fees?

Overall, on pure platform cost, the app-based players lead. Specifically, Trading 212, Lightyear and InvestEngine all charge no platform fee, while Freetrade's Basic plan is also free. Lightyear then edges ahead on overseas trades with its 0.10% FX fee, and InvestEngine removes FX fees altogether for its ETF range. Lightyear is also the platform we run our AI investing experiment on, so we see those low costs in practice.

However, "lowest fee" is not the whole story. For a large, fund-only pot, Vanguard's £375 cap can work out cheaper than a percentage charge elsewhere. Meanwhile, the managed options cost more on purpose, because you are paying for someone to run the portfolio. As a result, the cheapest platform on paper is not always the best investment ISA for your situation.

Other options worth knowing

In addition, two more are worth a mention beyond the main seven. First, Monzo Invest lets you open a stocks and shares ISA inside the Monzo app and invest in BlackRock managed funds from just £1, which suits total beginners who want set-and-forget simplicity. Its fee is 0.25% a year, or 0.20% on a paid Monzo plan, capped at £250. For background, see our note on Monzo's investment fee cut.

Second, Robinhood UK runs a low-cost ISA, but it only offers US-listed stocks, and its brokerage assets sit under US custody rather than standard UK FSCS investment protection. So it is a niche pick for US-focused investors who have read the terms. In both cases, capital is at risk and your investments can fall.

Limitations to weigh up

No investment ISA is flawless, so it pays to be clear-eyed. Above all, capital is at risk on every platform here, which means your balance can fall as well as rise. For money you need soon, a cash ISA may suit you better.

There are smaller catches too. For instance, the "free" apps still charge FX on overseas shares, which adds up if you trade US stocks often. The managed options, namely Monzo Invest and J.P. Morgan, cost more and give you less control. Vanguard's small-pot minimum fee can bite. Finally, InvestEngine limits you to ETFs. In short, the right pick follows your goals, not a single league table.

What is changing from April 2027?

Looking ahead, the rules shift for the 2027/28 tax year, which starts on 6 April 2027. From then, the amount under-65s can pay into a cash ISA falls to £12,000, while savers aged 65 and over keep the full £20,000 cash allowance. The government announced this in the Autumn 2025 Budget, and you can track the detail through MoneyHelper's ISA guide.

Importantly, the overall £20,000 ISA allowance stays the same. So for under-65s, the remaining £8,000 can still go into a stocks and shares ISA. As a result, 2026/27 is the last full year with the £20,000 cash flexibility, which is one more reason to weigh up a stocks and shares ISA now. For a cash-versus-investing view, our guide to the best savings options for the new tax year goes deeper.

FAQs: best investment ISA 2026

What is the best investment ISA in 2026?

There is no single best investment ISA, because it depends on your style. For low-cost global investing, Lightyear stands out. For a wide DIY range, Trading 212 is strong. For hands-off investing, Monzo Invest or J.P. Morgan suit better. So match the platform to how you actually invest.

Stocks and shares ISA vs cash ISA, which should I pick?

It depends on your time frame. A cash ISA is lower risk and suits money you need within a few years. A stocks and shares ISA has more growth potential over five years or more, but its value can fall. Many people use both, splitting one £20,000 allowance between them.

How much can I put in an ISA this year?

You can pay in up to £20,000 across your ISAs in the 2026/27 tax year. Moreover, you can split it between cash, stocks and shares, innovative finance and a Lifetime ISA (up to £4,000). Any unused allowance is lost after 5 April 2027, because it does not roll over.

Are investment ISAs safe and FSCS protected?

Investing always carries risk, so your balance can drop. However, if your platform is FCA-authorised, eligible investments are protected up to £85,000 per person per FCA-authorised firm by the FSCS. Importantly, that covers firm failure, not market losses. Robinhood is an exception to check, because its assets sit under US custody.

Which ISA has the lowest fees?

On platform fees, Trading 212, Lightyear and InvestEngine charge nothing, and Freetrade's Basic plan is free too. Lightyear leads on FX at 0.10%, while InvestEngine has no FX fee on ETFs. Still, check fund charges and FX, since those decide your real cost.

Can I open more than one stocks and shares ISA?

Yes. Since April 2024, you can pay into more than one ISA of the same type in the same tax year. So you could hold stocks and shares ISAs with, say, Lightyear and Trading 212 at once, as long as your total contributions stay within £20,000.

Not financial advice. This article is for information only and reflects personal experience, not a recommendation. Rates, fees, offers and terms can change, so always check the provider's current details and consider speaking to a qualified financial adviser before you invest. Capital at risk. The value of investments can go down as well as up and you may get back less than you invested. Past performance is not a reliable indicator of future results. Tax treatment depends on the individual circumstances of each client and may be subject to change in future. This article contains affiliate or referral links; if you click through and sign up I may earn a commission or referral bonus at no extra cost to you, and it does not affect my editorial view.

More from CoolCuration

- StockEvents app: track your whole portfolio, dividends and ISA in one tidy app.

- Monzo £5 to £50 referral: open a Monzo current account and get a randomly chosen welcome bonus.

- Best apps to save money: round-ups, pots and cashback tools to build your ISA deposits faster.

- Gifts for techies: present ideas for the gadget lover who already has everything.

- reMarkable Paper Pro: the paper tablet we rate for distraction-free planning and notes.

What's trending

Recent posts

- Which Huel to Buy? Every Huel Product Compared 2026

Which Huel to buy in 2026? We compare every Huel product, from Powder and Black Edition to Diet, bars and greens, with honest pros and cons.

Which Huel to buy in 2026? We compare every Huel product, from Powder and Black Edition to Diet, bars and greens, with honest pros and cons. - GTA 6 Pre-Order UK: Price, Editions and Where to BuyGTA 6 pre-orders are live in the UK. Here is the price, the Standard and Ultimate editions, the Vintage Vice City bonus and where to buy before 19 November 2026.

- EcoFlow Wave 3 ReviewMy honest EcoFlow Wave 3 review after a summer of daily use: the dual-hose portable air con that is quiet, tiny and cheap to run on Octopus.

No Comments.