Last updated: 19 July 2026

By Stiv · Design, technology and personal finance

Quick context before the verdict: I pay a Nationwide mortgage myself and have put £100 a month through Sprive since October 2021, so this opinion rests on over four years of actual overpayments rather than a quick trial.

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view.

Your home may be repossessed if you do not keep up repayments on your mortgage. CoolCuration is not authorised by the Financial Conduct Authority and this is not financial advice.

Thinking of trying Sprive?

If you decide to give the app a go, the current sign-up bonus and the steps to claim it are kept up to date on our referral page.

Claim the Sprive sign-up bonus

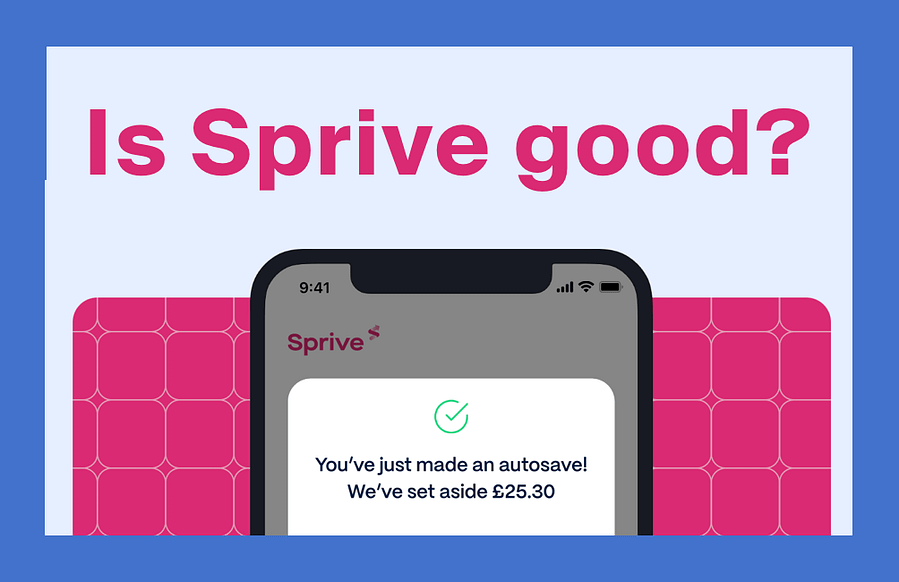

Is Sprive any good? That is the question most UK homeowners land on after hearing about the mortgage overpayment app for the first time. You have probably seen it on Dragons' Den, spotted it on Trustpilot, or had a friend mention it over a pint. In my experience, for many people with a mortgage who want to overpay but struggle to stay consistent, Sprive does the job well, though whether it suits you depends on your lender support and your habits. It is not magic, it is not going to halve your mortgage overnight, and it is not for everyone. But after using it since October 2021 with my Nationwide mortgage, making regular monthly overpayments, I think it earns its place on your phone. Here is why.

What Sprive actually does

Sprive is a free UK app that helps homeowners make small, regular mortgage overpayments without the monthly admin of setting up standing orders and remembering to adjust them. It connects to your bank through Open Banking, analyses your spending, and sets aside affordable amounts within limits you choose. You then send those amounts to your mortgage lender in a single tap.

On top of the overpayment side, there is a shopping feature. You buy digital gift cards for retailers like Tesco, Sainsbury's, Amazon, M&S, and over 1,000 brands in total through Sprive's partnership with Tillo, and earn cashback that gets routed straight into your mortgage pot. It sounds like a gimmick until you realise your weekly food shop is quietly chipping away at your balance.

Sprive supports 14 of the largest UK lenders, including Nationwide, Halifax, Barclays, HSBC, NatWest, and Santander. The full current list -- which includes First Direct, Lloyds, RBS, Virgin Money, TSB, Yorkshire Building Society, Coventry Building Society, and Accord Mortgages -- is on Sprive's FAQ page.

Why Sprive is worth considering

The reason Sprive is worth considering comes down to one thing: it makes a boring but important financial habit effortless. Most people know overpaying their mortgage saves money in the long run. The MoneyHelper overpayment guide explains how even small extra payments can knock years off your term and save thousands in interest. The problem is that knowing and doing are two very different things. A standing order is rigid. Sprive adapts to your spending, so you are never overcommitting in a tight month.

After several years of using it, three things stand out:

Consistency without effort. The app quietly builds up overpayment amounts in the background. You approve or skip each payment, so you stay in control, but the default is progress rather than inertia.

Cashback that actually goes somewhere useful. Earning a few percent on your Tesco shop is not life-changing on its own. But when it compounds towards your mortgage balance every single week, it adds up faster than you would expect. Users who route their regular food shop through the app typically earn around £20 to £30 a month in cashback towards their mortgage.

Visibility. The app shows you how much interest you are projected to save and how many months you are shaving off your mortgage. That feedback loop is surprisingly motivating.

Where Sprive falls short

No app is perfect, and Sprive is not for everyone. Here is what holds it back:

Open Banking reconnection. Bank connections occasionally need refreshing. This is a common Open Banking quirk across all fintech apps, not a Sprive-specific fault, but it is still a mild annoyance when you have to re-authorise mid-week.

Gift card friction. The cashback feature works through digital gift cards, which means you need to buy them before you shop. At a supermarket checkout, that extra step takes a minute or two. Some users find it clunky, especially in stores with slow card readers.

Limited lender support. Fourteen lenders is a decent spread, but if your mortgage is with a smaller building society or a specialist lender, you may not be able to use Sprive at all. Check before you download.

Safeguarded, not FSCS-protected. Money held in your Sprive wallet sits with an e-money provider (PrePay Technologies Limited, FRN 900010, authorised by the FCA under the Electronic Money Regulations 2011). Funds are safeguarded, meaning they are kept separate from Sprive's own money, but they are not covered by the Financial Services Compensation Scheme the way a bank deposit would be. For most users this is fine because the amounts are small and move quickly towards your lender, but it is worth understanding. We cover this in detail in our Sprive safety breakdown.

Who Sprive suits

Sprive works best if you are a UK homeowner who wants to overpay your mortgage but finds it hard to stay consistent. If you already have a disciplined standing order and never miss a month, you probably do not need an app to do what willpower already handles. But if you are the sort of person who means to overpay and then forgets, or whose spare cash varies month to month, Sprive fills that gap well.

It is also a solid pick if you do most of your shopping at the supported retailers and want those small cashback amounts to go somewhere meaningful rather than sitting in a loyalty app you never check.

Who should skip it

If your lender is not supported, there is no workaround. If you are on a tight fixed-rate deal with strict early repayment charges, check your overpayment allowance first. Most UK mortgages allow overpayments of up to 10% of the outstanding balance per year without penalties, but you should confirm this with your lender before setting anything up.

If you want a comprehensive walkthrough of how the app works day to day, read our full Sprive mortgage app review. For the step-by-step setup process, head to our guide on how the Sprive app works.

Trustpilot, Dragons' Den, and credibility

Sprive currently holds a 4.6 out of 5 rating on Trustpilot from over 900 reviews. The most common praise is around ease of use and the cashback feature. The most common complaint is occasional slow gift card delivery and customer service response times.

In February 2026, Sprive appeared on BBC Dragons' Den (Series 23). Three Dragons invested, which is a useful signal of commercial credibility, though it is not a guarantee of product quality.

Sprive Limited (FRN 919863) is an appointed representative of Connect IFA Ltd (FRN 441505) and New Leaf Distribution Limited (FRN 460421) for mortgage services, both authorised and regulated by the Financial Conduct Authority. You can verify Sprive on the FCA Register (Sprive Limited 919863), Connect IFA on the FCA Register (Connect IFA Ltd 441505), and New Leaf Distribution on the FCA Register (New Leaf Distribution Limited 460421).

How to try Sprive

If you want to give it a go, you can sign up using referral code LM125CR6 to get the current sign-up reward. Full details and claim steps are on our Sprive referral code page.

Get the Sprive sign-up bonusThe bottom line

Is Sprive any good? For most UK homeowners who want to overpay their mortgage without relying on willpower alone, yes. It is not flashy, it will not transform your finances overnight, and the gift card process could be smoother. But it removes friction from a habit that genuinely saves you money over time. If you are already thinking about overpaying, Sprive makes it easier to actually do it.

Disclaimer: This article is for information only and is not financial advice. Always check your mortgage terms, overpayment limits, and the app's current features before making decisions. Some links on this page are referral or affiliate links. If you sign up through them, CoolCuration may earn a commission at no extra cost to you.

Frequently asked questions

Is Sprive any good for small overpayments?

Yes. Sprive is designed around small, regular amounts rather than large lump sums. Even £25 to £50 a month in overpayments can reduce your mortgage term and save you interest over time. The app lets you set minimum and maximum saving limits so you stay comfortable.

Is Sprive free to use?

The core app is free. Sprive makes money through cashback commissions from retailers and mortgage broking fees if you remortgage through them. You are never charged for making overpayments.

Is Sprive better than a standing order?

It depends on your personality. A standing order is predictable and simple. Sprive is flexible and adapts to your spending. If your income or outgoings vary month to month, Sprive handles that better than a fixed amount. If you are already disciplined and consistent, a standing order does the job. We compare both approaches in our Sprive vs manual overpaying guide.

Does Sprive work with my mortgage lender?

Sprive supports 14 major UK lenders including Nationwide, Halifax, Barclays, HSBC, NatWest, Santander, Lloyds, TSB, Virgin Money, Yorkshire Building Society, Coventry Building Society, Accord Mortgages, RBS, and First Direct. If your lender is not on the list, you cannot use the app at present.

Is the cashback feature worth it?

If you already shop at the supported retailers (and most people do for groceries), yes. The amounts per transaction are small, but they compound over weeks and months. Users who route their regular food shop through the app typically earn around £20 to £30 a month in cashback towards their mortgage.

How is Sprive regulated?

Sprive Limited (FRN 919863) is an appointed representative of Connect IFA Ltd (FRN 441505) and New Leaf Distribution Limited (FRN 460421), both authorised and regulated by the FCA. You can verify this on the FCA Register. Money held in the app sits with PrePay Technologies Limited (FRN 900010), an FCA-authorised e-money institution. Funds are safeguarded but not FSCS-protected. For a full breakdown, read our Is Sprive safe? guide.

More from CoolCuration

- Best cashback apps UK -- The top cashback apps for earning money back on everyday spending in 2026.

- How to cut household bills -- Practical ways to reduce your monthly outgoings without changing your lifestyle.

- Best mortgage overpayment apps UK -- How Sprive compares to Chip, Plum, and other tools.

- Sprive cashback explained -- Gift card mechanics, checkout tips, and when the cashback is worth the effort.

- How to pay off your mortgage faster -- Seven practical moves that save thousands.

What's trending

Recent posts

- Best Free Budgeting Apps UK 2026

The best free budgeting apps in the UK for 2026, compared: what each free tier really includes, what is paywalled, and who each app suits.

The best free budgeting apps in the UK for 2026, compared: what each free tier really includes, what is paywalled, and who each app suits. - InvestEngine Review: My Honest Take After Six MonthsMy honest InvestEngine review after six months: no-fee ETF investing, the real bonus odds, and who this low-cost UK platform actually suits.

- Best Current Account UK 2026: Ranked and ComparedCurrent accounts2026 Edit The best current account is the one you actually enjoy opening Picking the best current account in 2026 is no longer just about interest. It is about the app you tap ten times a day, the perks that quietly pay you back, and the switch bonus that lands in a week. So… Read more: Best Current Account UK 2026: Ranked and Compared

No Comments.