Last updated: 19 July 2026

By Stiv · Design, technology and personal finance

This is an opinion piece. Views expressed are the author's own and do not constitute professional advice.

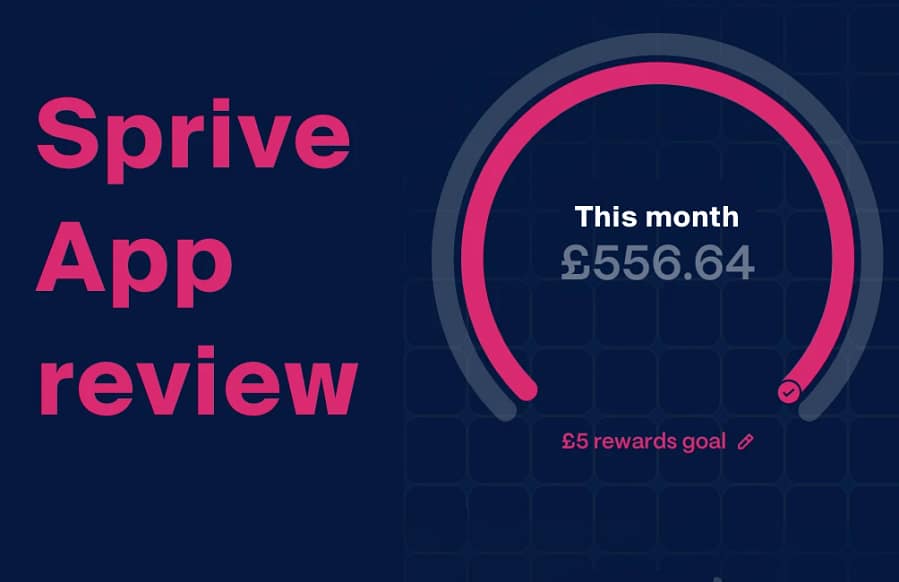

I've been using Sprive with my Nationwide mortgage since October 2021, making £100 monthly overpayments through the app's auto-save feature. In that time I've overpaid a total of £3,294.55, including cashback from Shop with Sprive on our weekly shops. This review is based on over four years of real, daily use.

If you're looking for a realistic way to make progress on your mortgage without committing to rigid overpayments, the Sprive mortgage app is one of the better-known tools in the UK. Sprive has also pushed further into the mainstream in 2026, with a TV advert running on Channel 4 under the line "Shop away your mortgage. Brick by brick." This Sprive mortgage app review focuses on what actually matters: how it works in day-to-day use, who it's good for, and where it falls short. It's not a sales pitch, and it's not a deep dive into regulation or bonuses. If you're mainly concerned about security and FCA regulation, we cover that separately: Is Sprive safe?

This article contains affiliate or referral links. If you click through and sign up I may earn a commission or referral bonus at no extra cost to you. It does not affect my editorial view. CoolCuration is not authorised by the Financial Conduct Authority, and this is an opinion, not financial advice.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Short on time?

The current Sprive sign-up bonus and how to claim it are kept up to date on one page.

Claim the Sprive referral bonus

Cool Factor

★★★★☆

4 out of 5